HSBC 2011 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

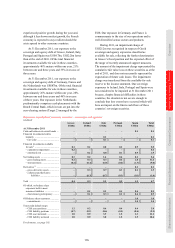

113

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

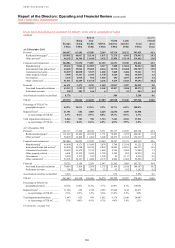

officials. This process enabled us to form a view of

the credit standing and the level of exposure that

the counterparties have to peripheral eurozone

sovereigns and banks. The majority of these

counterparties are located in France, Germany and

the Netherlands, where the exposures are disclosed

in aggregate below. Vulnerable counterparties were

identified, subject to enhanced monitoring and our

exposure was managed in a way similar to the

monitoring and management of direct exposures to

the peripheral eurozone countries.

The overall quality of the portfolio was strong

with most in-country and cross-border limits

extended to countries with high-grade internal credit

risk ratings. We regularly update our assessment of

higher risk countries and adjust our risk appetite

accordingly.

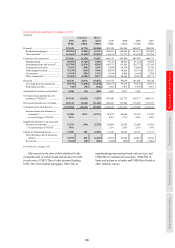

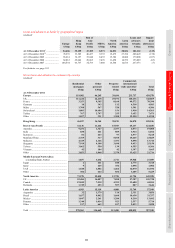

Exposures to countries in the eurozone

(Unaudited)

2011 was a turbulent year for the global markets,

dominated by the continuing eurozone debt crisis that

started with the global financial crisis in 2007 and,

by 2011, had developed into a severe sovereign debt

crisis. The measures taken by governments during

that period to avoid a financial collapse resulted in

higher debt levels, large fiscal deficits and, in certain

cases, social and political disruption. During 2011, a

number of eurozone countries came under severe

financial pressure and their ability to raise, refinance

and service their debt was put into question by

markets, as demonstrated by the record high spreads

during most of the year. Greece, Ireland and Portugal

were forced to seek support packages from the

European Central Bank (‘ECB’) and the International

Monetary Fund (‘IMF’) under strict conditions, while

fear of contagion to other eurozone countries forced

governments to reduce debt levels through austerity

measures that, at least in the short term, were seen

as the cause of slow growth for some countries and

stagnation in others.

Despite a number of high profile summits and

meetings the EU was unable to agree and implement

a strong coherent policy response to the crisis,

prompting fear of default or the exit from the euro of

one or more members. Under pressure during most of

2011, EU members showed an increasing willingness

to agree a structured common approach, but they also

demonstrated divergent opinions on the way forward

and on the measures to be taken. This resulted in the

three major rating agencies either downgrading, or

putting on the watch list for possible downgrade, a

number of sovereigns which intensified the pressure,

even on the stronger eurozone countries.

The ongoing sovereign debt crisis, slow

economic growth, dearth of market financing for

banks and private sector deleveraging severely

affected the eurozone financial system, increasing

the possibility of further banking stress in the region.

The banking sector within the peripheral eurozone

countries was particularly under threat as the credit

risk of domestic and cross-border exposures

increased significantly. This prompted calls from the

European Banking Authority (‘EBA’) and the IMF

for funding and liquidity support and/or the

recapitalisation of certain European banks.

The ratings downgrade of a number of eurozone

countries by major rating agencies in 2011 and

January 2012 was generally anticipated and was, in

most cases, not as large as feared, with the exception

of Portugal which is now rated below investment

grade. The downgrades are likely to have

implications for the ratings of European banks and

government guaranteed securities, as evidenced by

the downgrade of the European Financial Stability

Fund (‘EFSF’).

We continue to closely monitor events and have

stress-tested our capital position for potential

scenarios.

The tables below summarise our exposures to

selected eurozone countries, including:

• governments and central banks of selected

eurozone countries along with near/quasi

government agencies;

• banks; and

• other financial institutions and other corporates.

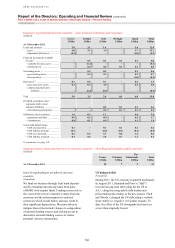

Exposures to banks, other financial institutions

and other corporates are based on the country of

domicile of the counterparty.

The following analysis of our exposures to

selected European countries is made voluntarily to

reflect developments in best practice disclosure.

Whilst certain analysis is subject to audit and

incorporated into the Group’s risk management

disclosure, it is not required for the purposes of

compliance with IFRSs.

Basis of preparation

(Audited)

The countries presented were selected as they

exhibited levels of market volatility during 2011

which exceeded other eurozone countries and

demonstrated fiscal or political uncertainty. Certain

of these countries also have high sovereign debt to

GDP ratios and a short to medium-term maturity

concentration of those liabilities.