HSBC 2011 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

33

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

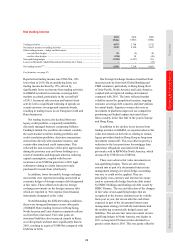

Movement in 2011

Total reported assets were US$2.6 trillion, 4%

higher than at 31 December 2010. Excluding the

effect of currency movements, total assets increased

by 6%.

Strong growth in deposits across most regions

enabled us to support our customers’ borrowing

requirements, leading to significantly higher term

lending and mortgage balances in Hong Kong, Rest

of Asia-Pacific and the UK. Our strong liquidity

position and risk preference also led to a rise in

balances at central banks. In addition, the fair value

of derivative contracts increased markedly, as the

deteriorating economic outlook resulted in a decline

in yield curves in major currencies during the latter

part of the year. This growth was offset in part by a

reduction in net trading assets as we took action to

manage our balance sheet more effectively, which

resulted in year-end balances being lower than the

average for the year.

The following commentary is based on a

comparison with the balance sheet at 31 December

2010 as shown on page 35.

Assets

Cash and balances at central banks rose by 129%.

The increasingly prominent role played by western

central banks in the functioning of the money

markets as well as our own risk preference as the

eurozone crisis deepened resulted in a larger portion

of our excess liquidity being held with central banks

in Europe and in North America. The redeployment

of funds from maturities and sales of financial

investments and strong growth in deposits also

contributed to the rise.

Trading assets decreased by 13%. Economic

uncertainty led to a decline in market activity. As a

result, we reduced our holdings of government and

highly-rated corporate debt securities and equity

positions, notably in Europe, and did not replace

maturities in our reverse repo book. This was partly

offset by higher cash collateral posted with external

counterparties as the fair value of derivative

liabilities rose.

Financial assets designated at fair value

declined by 14% as a result of improved netting of

assets and the associated non-recourse liabilities.

There was a corresponding reduction in ‘Financial

liabilities designated at fair value’.

Derivative assets increased by 35%, due to a

significant rise in the fair value of interest rate

contracts in Europe. This was driven by the

downward movements of yield curves in major

currencies following the global monetary response to

continued economic weakness, including

quantitative easing measures. The notional value of

contracts outstanding also increased, reflecting a

higher number of open interest rate and foreign

exchange transactions than a year ago. The increase

in the fair value of derivative assets was partly offset

by higher netting, which rose in line with the

increase in fair values.

Loans and advances to banks declined by 11%,

as funds from maturing term loans and reverse repo

balances, notably in Europe, were redeployed to

‘Cash and balances at central banks’. This was offset

in part by higher central bank lending in Rest of

Asia-Pacific, reflecting strong deposit growth in the

region.

Loans and advances to customers were broadly

in line with 2010. Following the announcement of

agreements for the sale of 195 non-strategic US

branches and our Cards and Retail Services business,

we reclassified the related loans and advances to

‘Assets held for sale’, which, for the purpose of this

commentary, is reported within ‘Other assets’ (see

page 86). We also reclassified loans and advances

relating to the planned disposals of non-strategic

banking operations in Central America, the RBWM

business in Thailand and our private banking

business in Japan to ‘Assets held for sale’.

Excluding the above reclassifications, loans and

advances to customers increased by US$30bn

compared with 2010, although the pace of growth

slowed in the second half of 2011. This reflected

targeted loan growth in our CMB and GB&M

businesses in Hong Kong and Rest of Asia-Pacific as

the economic environment improved and trade flows

increased, together with growth as a result of lending

campaigns in CMB in the UK and Latin America.

Residential mortgage balances also rose significantly

in the UK, Hong Kong and Rest of Asia-Pacific due

to a strong sales focus and competitive pricing,

reflecting the successful implementation of our

strategy to reposition RBWM towards higher quality

secured lending. This growth was offset in part by a

reduction in reverse repo balances in Europe and

North America, as a result of lower market activity.

Financial investments were broadly in line with

2010, as Balance Sheet Management continued to

hold large portfolios of highly liquid assets. In North

America, financial investments rose due to the

purchases of government and government agency

debt securities. This was partly offset by a reduction

in Europe, where a portion of the proceeds from

sales and maturities of financial investments were

placed at central banks.