HSBC 2011 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

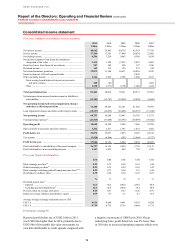

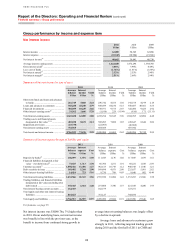

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Financial summary > Group performance

28

settlement accounts) compared with 2.2% at

31 December 2010.

In 2011, loan impairment charges and other

credit risk provisions declined in all regions except

Latin America and Hong Kong. The reduction was

most significant in our consumer finance portfolios

in HSBC Finance in North America, which

contributed 66% of the reduction, reflecting lower

lending balances in the run-off portfolio along with a

reduction in lending balances and lower delinquency

rates as our Card and Retail Services customers

focused on repayments. In Latin America, principally

Brazil, and also in Hong Kong, collective loan

impairment allowances rose as we grew our lending

book on the back of strong economic growth and

increased customer demand.

During 2011, we reported US$631m of

impairments related to available-for-sale debt

securities, compared with US$472m in 2010. In

2011, we recognised a charge of US$212m to write

down to market value available-for-sale Greek

sovereign debt now judged to be impaired following

the deterioration in Greece’s fiscal position. This was

partly offset as losses arising in underlying collateral

pools generated lower charges on asset-backed

securities.

In our US run-off portfolios, loan impairment

charges of US$5.0bn were 14% lower than in 2010.

The decline was mainly in our Consumer and

Mortgage Lending (‘CML’) portfolio, driven by the

reduction in customer lending balances, in part offset

by higher loan impairment allowances reflecting a

rise in the estimated cost to obtain collateral as well

as delays in the timing of expected cash flows, both

the result of the industry-wide delays in foreclosure

processing.

In the third quarter of 2011, loan impairment

charges in the CML portfolio increased markedly as

delinquency worsened compared with the first half of

2011. In addition, we increased our loan impairment

allowances to reflect a rise in the expected cost to

obtain and realise collateral following delays in

foreclosure processing. Despite a decline in loan

impairment charges in the fourth quarter, these

factors contributed significantly to a rise in the

Group’s loan impairment charges in the second half

of 2011 compared with the first half of the year.

In Card and Retail Services, loan impairment

charges fell by 26% to US$1.6bn reflecting lower

lending balances and improved delinquency rates as

customer repayment rates remained strong during

2011.

In CMB, loan impairment charges and other

credit risk provisions in North America declined in

both Canada and the US reflecting improved credit

quality, and in Canada this was also due to lower

lending balances. These declines were partly offset

by a loan impairment charge on a commercial real

estate lending exposure.

The reduction in loan impairment charges and

other credit risk provisions in North America was

partly offset by an increase in GB&M, reflecting

lower releases of collective loan impairment

allowances compared with 2010. In addition, 2011

included a loan impairment charge associated with a

corporate lending relationship.

Loan impairment charges and other credit risk

provisions in Europe fell by 20% to US$2.5bn,

notably in the UK. The reduction was mainly in our

RBWM business where loan impairment charges

declined by 53% to US$596m despite the difficult

economic climate and continued pressures on

households’ finances. Delinquency rates declined

across both the secured and unsecured lending

portfolios, reflecting improvement in portfolio

quality and the continued low interest rate

environment as well as successful actions taken to

mitigate credit risk and proactive account

management. In CMB, loan impairment charges and

other credit risk provisions were 7% lower, mainly in

the UK. This was partly offset by an increase in

individually assessed loan impairment charges in

Greece as economic conditions worsened.

In GB&M in Europe, loan impairment charges

and other credit risk provisions increased by 8% as

we recorded an impairment of US$145m to write

down to market value available-for-sale Greek

sovereign debt now judged to be impaired following

the deterioration in Greece’s fiscal position. Further

information on our exposures to countries in the

eurozone is provided in ‘Areas of special interest –

wholesale lending’ on page 112.

In the Middle East and North Africa, loan

impairment charges and other credit risk provisions

fell by 53% to US$293m, primarily due to a marked

decline in loan impairment charges and other credit

risk provisions in our GB&M business. This

reflected the non-recurrence of individually assessed

loan impairment charges recorded in the first half of

2010 related to restructuring activity for a small

number of large corporate customers in the United

Arab Emirates (‘UAE’). In RBWM, loan impairment

charges declined by 45%, due to significantly

improved delinquency rates reflecting a repositioning

of the loan book towards higher quality lending as