Chrysler 2014 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2014 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

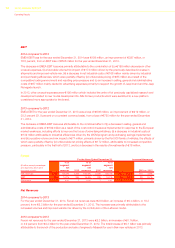

2014 | ANNUAL REPORT 69

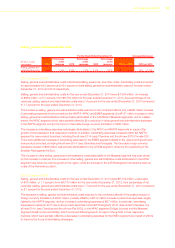

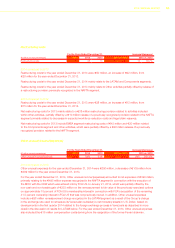

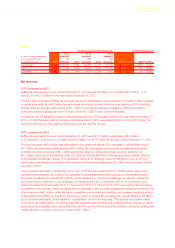

LATAM

For the Years Ended December 31, Increase/(decrease)

(€ million, except

percentages and

shipments which are

in thousands of units) 2014

% of

segment

net

revenues 2013

% of

segment

net

revenues 2012

% of

segment

net

revenues 2014 vs. 2013 2013 vs. 2012

Net revenues 8,629 100.0% 9,973 100.0% 11,062 100.0% (1,344) (13.5)% (1,089) (9.8)%

EBIT 177 2.1% 492 4.9% 1,025 9.3% (315) (64.0)% (533) (52.0)%

Shipments 827 n.m 950 n.m. 979 n.m. (123) (12.9)% (29) (3.0)%

Net revenues

2014 compared to 2013

LATAM net revenues for the year ended December 31, 2014 were €8.6 billion, a decrease of €1.3 billion, or

13.5 percent (6.9 percent on a constant currency basis), from €10.0 billion for the year ended December 31, 2013.

The total decrease of €1.3 billion was attributable to (i) a decrease of €1.2 billion driven by lower shipments, and (ii)

unfavorable foreign currency translation of €0.7 billion, which were partially offset by (iii) favorable net pricing and

vehicle mix of €0.6 billion.

The 12.9 percent decrease in vehicle shipments from 950 thousand units for the year ended December 31, 2013, to

827 thousand units for the year ended December 31, 2014 reflected the weaker demand in the region’s main markets,

where Brazil continued the negative market trend started in 2012, Argentina was impacted by import restrictions and

additional tax on more expensive vehicles and Venezuela suffered from weaker trading conditions. The weakening

of the Brazilian Real against the Euro impacted net revenues by €0.6 billion, in particular, the average exchange rate

used to translate Brazilian Real balances for the year ended December 31, 2014, was 8.9 percent lower than the

average exchange rate used for the same period in 2013.

2013 compared to 2012

LATAM net revenues for the year ended December 31, 2013 were €10.0 billion, a decrease of €1.1 billion, or 9.8

percent (an increase of 0.7 percent on a constant currency basis), from €11.1 billion for the year ended December

31, 2012. The total decrease of €1.1 billion was attributable to the combination of the impact of (i) unfavorable foreign

currency translation of €1.2 billion, and (ii) €0.3 billion related to a decrease in vehicle shipments, which were partially

offset by (iii) favorable mix of €0.1 billion and (iv) favorable pricing impact of €0.1 billion.

LATAM net revenues were significantly impacted by the weakening of the Brazilian Real against the Euro, as the

average exchange rate used to translate 2013 balances was 14.3 percent lower than the average exchange rate

for 2012, impacting net revenues negatively by €1.2 billion. The 3.0 percent vehicle shipment decrease from

979 thousand units for 2012 to 950 thousand units for 2013, which impacted net revenues by €0.3 billion, was largely

attributable to reductions of shipments in Brazil. In 2012 sales tax incentives were introduced to promote the sale of

small vehicles, a segment in which we hold a market leading position. As such, we were well positioned to meet the

increased consumer demand for small cars, recording an increase in shipments in 2012. In 2013, the gradual phase

out of the tax incentives was initiated and was a contributing factor to a shift in market demand away from the small

car segment and into larger vehicles, resulting in a decrease in our Brazilian market share, from 23.3 percent in 2012

to 21.5 percent in 2013.