Chrysler 2014 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2014 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

2014 | ANNUAL REPORT 177

The fair value of the options was calculated as the difference between the estimated exercise price for the disputed

options encompassed in the Equity Purchase Agreement of U.S.$650 million (€481 million) and the estimated fair

value for the underlying approximately 10 percent interest in FCA US of U.S.$952 million (€704 million). The exercise

price for the disputed options was originally calculated by FCA NA pursuant to the formula set out in the option

agreement between FCA NA and the VEBA Trust. The VEBA Trust disputed the calculation of the exercise price,

which ultimately led to the litigation between the two parties regarding the interpretation of the call option agreement.

The dispute primarily related to four elements of the calculation of the exercise price. During the ensuing litigation,

the court ruled in FCA NA’s favor on two of the four disputed elements of the calculation. The court requested an

additional factual record be developed on the other two elements, a process that was ongoing at the time the Equity

Purchase Agreement was executed and consummated.

The dispute between FCA NA and the VEBA Trust over the previously exercised options was settled pursuant to

the Equity Purchase Agreement, effectively resulting in the fulfillment of the previously exercised options. Given that

there was no amount explicitly agreed to by FCA NA and the VEBA Trust in the Equity Purchase Agreement for

the settlement of the previously exercised options, management estimated the exercise price encompassed in the

Equity Purchase Agreement taking into account the judgments rendered by the court to date on the litigation and

a settlement of the two unresolved elements. Based on the nature of the two unresolved elements, management

estimated the exercise price to be between U.S.$600 million (€444 million at the transaction date) and U.S.$700

million (€518 million at the transaction date). Given the uncertainty inherent in court decisions, it was not possible to

pick a point within that range that represented the most likely outcome. As such, management believed the mid-point

of this range, U.S.$650 million (€481 million at the transaction date), represented the appropriate point estimate of the

exercise price encompassed in the Equity Purchase Agreement.

Since there was no publicly observable market price for FCA US’s membership interests, the fair value as of the

transaction date of the approximately 10 percent non-controlling ownership interest in FCA US was determined

based on the range of potential values determined in connection with the IPO that FCA US was pursuing at the time

the Equity Purchase Agreement was negotiated and executed, which was corroborated by a discounted cash flow

valuation that estimated a value near the mid-point of the range of potential IPO values. Management concluded that

the mid-point of the range of potential IPO value provided the best evidence of the fair value of FCA US’s membership

interests at the transaction date as it reflects market input obtained during the IPO process, thus providing better

evidence of the price at which a market participant would transact consistent with IFRS 13 - Fair Value Measurement.

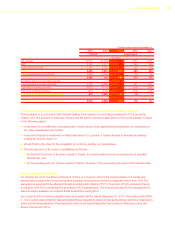

The potential IPO values for 100.0 percent of FCA US’s equity on a fully distributed basis ranged from $10.5 billion to

U.S.$12.0 billion (€7.6 billion to €8.7 billion at December 31, 2013). Management concluded the mid-point of this range,

U.S.$11.25 billion (€8.16 billion at December 31, 2013), was the best point estimate of fair value. The IPO value range

was determined using earnings multiples observed in the market for publicly traded US-based automotive companies

using the key assumptions discussed below. This fully distributed value was then reduced by approximately 15.0 percent

for the expected discount that would have been realized in order to complete a successful IPO for the minority interest

being sold by the VEBA Trust. This discount was estimated based on the following factors that a market participant

would have considered and, therefore, would have affected the price of FCA US’s equity in an IPO transaction:

Fiat held a significant controlling interest and had expressed the intention to remain and act as the majority owner

of FCA US. The fully diluted equity value, which is the starting point for the valuation discussed above, does not

contemplate the perpetual nature of the non-controlling interest that would have been offered in an IPO or the

significant level of control that Fiat would have exerted over FCA US. This level of control creates risk to a non-

controlling shareholder since Fiat would be able to make decisions to maximize its value in a manner that would not

necessarily maximize value to non-controlling shareholders, which Fiat had indicated was its intention.

The fully distributed equity value contemplates an active market for Chrysler’s equity, which did not exist for FCA

US’s membership interests. The IPO price represents the creation of the public market, which would have taken

time to develop into an active market. The estimated price that would be received in an IPO transaction reflects the

fact that FCA US’s equity was not yet traded in an active market.

As the expected discount that would have been realized in order to complete a successful IPO represented a market-

based discount that would have been reflected in an IPO price, management concluded it should be included in the

measurement at the transaction date between a willing buyer and willing seller under the principles in IFRS 13.