Chrysler 2014 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2014 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

46 2014 | ANNUAL REPORT

Overview of Our Business

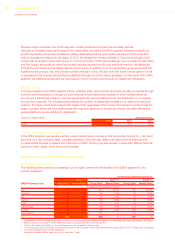

The following table presents our new vehicle market share information and our principal competitors in the U.S.,

our largest market in the NAFTA segment (certain totals in the tables included in this document may not add due to

rounding):

For the Years Ended December 31,

U.S. 2014 2013 2012

Automaker Percentage of industry

GM 17.4% 17.6% 17.6%

Ford 14.7% 15.7% 15.2%

Toyota 14.1% 14.1% 14.1%

FCA 12.4% 11.4% 11.2%

Honda 9.2% 9.6% 9.6%

Nissan 8.2% 7.9% 7.7%

Hyundai/Kia 7.8% 7.9% 8.6%

Other 16.2% 15.9% 16.0%

Total 100.0% 100.0% 100.0%

U.S. automotive market sales have steadily improved after a sharp decline from 2007 to 2010. U.S. industry sales,

including medium- and heavy-duty vehicles, increased from 10.6 million units in 2009 to 16.8 million units in 2014,

an increase of approximately 58.5 percent. Both macroeconomic factors, such as growth in per capita disposable

income and improved consumer confidence, and automotive specific factors, such as the increasing age of vehicles in

operation, improved consumer access to affordably priced financing and higher prices of used vehicles, contributed to

the strong recovery.

Our vehicle line-up in the NAFTA segment leverages the brand recognition of the Chrysler, Dodge, Jeep and

Ram brands to offer cars, utility vehicles, pick-up trucks and minivans under those brands, as well as vehicles in

smaller segments, such as the mini-segment Fiat 500 and the small & compact MPV segment Fiat 500L. With the

reintroduction of the Fiat brand in 2011 and the launch of the Dodge Dart in 2012, we now sell vehicles in all vehicle

segments. Our vehicle sales and profitability in the NAFTA segment are generally weighted towards larger vehicles

such as utility vehicles, trucks and vans, while overall industry sales in the NAFTA segment generally are more

evenly weighted between smaller and larger vehicles. In recent years, we have increased our sales of mini, small and

compact cars in the NAFTA segment.

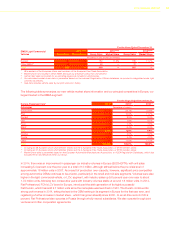

NAFTA Distribution

In the NAFTA segment, our vehicles are sold primarily to dealers in our dealer network for sale to retail customers and

fleet customers. The following table sets forth the number of independent entities in our dealer and distributor network

in the NAFTA segment. The table counts each independent dealer entity, regardless of the number of contracts or

points of sale the dealer operates. Where we have a relationship with a general distributor, this table reflects that

general distributor as one distribution relationship:

Distribution Relationships At December 31,

2014 2013 2012

NAFTA 3,251 3,204 3,156

In the NAFTA segment, fleet sales in the commercial channel are typically more profitable than sales in the government

and daily rental channels since they more often involve customized vehicles with more optional features and

accessories; however, vehicle orders in the commercial channel are usually smaller in size than the orders made in

the daily rental channel. Fleet sales in the government channel are generally more profitable than fleet sales in the

daily rental channel primarily due to the mix of products included in each respective channel. Rental car companies,

for instance, place larger orders of small and mid-sized cars and minivans with minimal options, while sales in the

government channel often involve a higher mix of relatively more profitable vehicles such as pick-up trucks, minivans

and large cars with more options.