Chrysler 2014 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2014 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

250 2014 | ANNUAL REPORT

Consolidated

Financial Statements

Notes to the Consolidated

Financial Statements

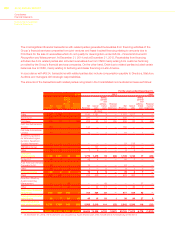

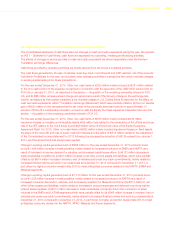

35. Qualitative and quantitative information on financial risks

The Group is exposed to the following financial risks connected with its operations:

credit risk, arising both from its normal commercial relations with final customers and dealers, and its financing

activities;

liquidity risk, with particular reference to the availability of funds and access to the credit market and to financial

instruments in general;

financial market risk (principally relating to exchange rates, interest rates and commodity prices), since the Group

operates at an international level in different currencies and uses financial instruments which generate interests. The

Group is also exposed to the risk of changes in the price of certain commodities and of certain listed shares.

These risks could significantly affect the Group’s financial position and results, and for this reason the Group

systematically identifies, and monitors these risks, in order to detect potential negative effects in advance and take the

necessary action to mitigate them, primarily through its operating and financing activities and if required, through the

use of derivative financial instruments in accordance with established risk management policies.

Financial instruments held by the funds that manage pension plan assets are not included in this analysis (see Note 25).

The following section provides qualitative and quantitative disclosures on the effect that these risks may have upon the

Group. The quantitative data reported in the following does not have any predictive value, in particular the sensitivity

analysis on finance market risks does not reflect the complexity of the market or the reaction which may result from

any changes that are assumed to take place.

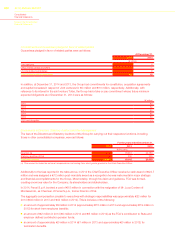

Credit risk

Credit risk is the risk of economic loss arising from the failure to collect a receivable. Credit risk encompasses the

direct risk of default and the risk of a deterioration of the creditworthiness of the counterparty.

The Group’s credit risk differs in relation to the activities carried out. In particular, dealer financing and operating and

financial lease activities that are carried out through the Group’s financial services companies are exposed both to the

direct risk of default and the deterioration of the creditworthiness of the counterparty, while the sale of vehicles and

spare parts is mostly exposed to the direct risk of default of the counterparty. These risks are however mitigated by the

fact that collection exposure is spread across a large number of counterparties and customers.

Overall, the credit risk regarding the Group’s trade receivables and receivables from financing activities is concentrated

in the European Union, Latin America and North American markets.

In order to test for impairment, significant receivables from corporate customers and receivables for which collectability

is at risk are assessed individually, while receivables from end customers or small business customers are grouped

into homogeneous risk categories. A receivable is considered impaired when there is objective evidence that the

Group will be unable to collect all amounts due specified in the contractual terms. Objective evidence may be provided

by the following factors: significant financial difficulties of the counterparty, the probability that the counterparty will

be involved in an insolvency procedure or will default on its installment payments, the restructuring or renegotiation

of open items with the counterparty, changes in the payment status of one or more debtors included in a specific

risk category and other contractual breaches. The calculation of the amount of the impairment loss is based on the

risk of default by the counterparty, which is determined by taking into account all the information available as to the

customer’s solvency, the fair value of any guarantees received for the receivable and the Group’s historical experience.

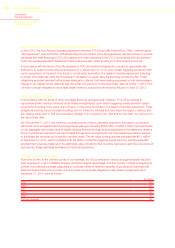

The maximum credit risk to which the Group is theoretically exposed at December 31, 2014 is represented by the

carrying amounts of financial assets in the financial statements and the nominal value of the guarantees provided on

liabilities and commitments to third parties as discussed in Note 33.