Chrysler 2014 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2014 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

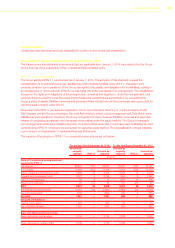

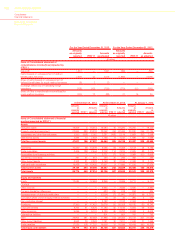

154 2014 | ANNUAL REPORT

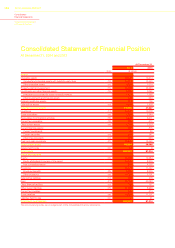

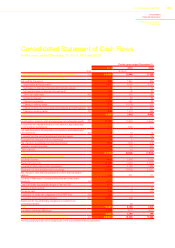

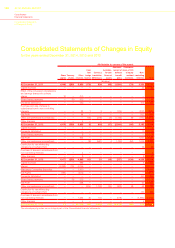

Consolidated

Financial Statements

Notes to the Consolidated

Financial Statements

Subsidiaries are deconsolidated from the date on which control ceases. When the Group ceases to have control

over a subsidiary, it de-recognizes the assets (including any goodwill) and liabilities of the subsidiary at their carrying

amounts at the date when control is lost, and de-recognizes the carrying amount of non-controlling interests in the

former subsidiary at the same date and recognizes the fair value of any consideration received from the transaction.

Any retained interest in the former subsidiary is remeasured to its fair value at the date when control is lost. This fair

value is the initial carrying amount for the purposes of subsequent accounting for the retained interest as an associate,

joint venture or financial asset. In addition, any amounts previously recognized in Other comprehensive income/(loss)

in respect of that entity are accounted for as if the Group had directly disposed of the related assets or liabilities.

This may mean that amounts previously recognized in Other comprehensive income/(loss) are reclassified to the

Consolidated income statement or transferred directly to retained earnings as required by other IFRS.

Interests in Joint Ventures and Associates

A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net

assets of the arrangement. Joint control involves the contractually agreed sharing of control of an arrangement, which

exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control.

An associate is an entity over which the Group has significant influence. Significant influence is the power to participate in

the financial and operating policy decisions of the investees but does not have control or joint control over those policies.

Joint ventures and associates are accounted for using the equity method of accounting from the date on which joint

control and significant influence is obtained. On acquisition of the investment, any excess of the cost of the investment

and the Group’s share of the net fair value of the investee’s identifiable assets and liabilities is recognized as goodwill

and is included in the carrying amount of the investment. Any excess of the Group’s share of the net fair value of the

investee’s identifiable assets and liabilities over the cost of the investment is included as income in the determination of

the Group’s share of the investee’s profit or loss in the acquisition period.

Under the equity method, the investments are initially recognized at cost, and adjusted thereafter to recognize the

Group’s share of the profit or loss and Other comprehensive income/(loss) of the investee. The Group’s share of the

investee’s profit or loss is recognized in the Consolidated income statement. Distributions received from an investee

reduce the carrying amount of the investment. Post-acquisition movements in Other comprehensive income/(loss)

are recognized in Other comprehensive income/(loss) with a corresponding adjustment to the carrying amount of

the investment.

Unrealized gains on transactions between the Group and its joint ventures and associates are eliminated to the extent

of the Group’s interest in the joint venture or associate. Unrealized losses are also eliminated unless the transaction

provides evidence of an impairment of the asset transferred.

When the Group’s share of the losses of a joint venture or associate exceeds the Group’s interest in that joint venture

or associate, the Group discontinues recognizing its share of further losses. Additional losses are provided for, and

a liability is recognized, only to the extent that the Group has incurred legal or constructive obligations or made

payments on behalf of the joint venture or associate.

The Group discontinues the use of the equity method from the date when the investment ceases to be an associate or

a joint venture or when it is classified as available-for-sale.