Chrysler 2006 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2006 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

|

|

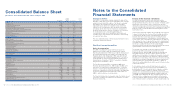

Fiat Group Consolidated Financial Statements at December 31, 2006 -Notes 101

2002 and not yet vested at January 1, 2005, the effective date

of the Standard. Detailed information is provided in respect of

all stock options granted on or prior to November 7, 2002.

Provisions

The Group records provisions when it has an obligation,

legal or constructive, to a third party, when it is probable that

an outflow of Group resources will be required to satisfy the

obligation and when a reliable estimate of the amount can

be made.

Changes in estimates are reflected in the income statement

in the period in which the change occurs.

Treasury shares

Treasury shares are presented as a deduction from equity.

The original cost of treasury shares and the proceeds of any

subsequent sale are presented as movements in equity.

Revenue recognition

Revenue is recognised if it is probable that the economic

benefits associated with the transaction will flow to the Group

and the revenue can be measured reliably.Revenues are stated

net of discounts, allowances, settlement discounts and rebates,

as well as costs for sales incentive programs, determined on

the basis of historical costs, country by country, and charged

against profit for the period in which the corresponding sales

are recognised. The Group’s incentive programs include the

granting of retail financing at significant discount to market

interest rates. The corresponding cost is recognised at the

time of the initial sale.

Revenues from the sale of products are recognised when the

risks and rewards of ownership of the goods are transferred

to the customer, the sales price is agreed or determinable and

receipt of payment can be assumed: this corresponds generally

to the date when the vehicles are made available to non-group

dealers, or the delivery date in the case of direct sales. New

vehicle sales with a buy-back commitment are not recognised

at the time of delivery but are accounted for as operating

leases when it is probable that the vehicle will be bought back.

The measurement of work in progress is based on the stage of

completion. These items are presented net of progress billings

received from customers. Any losses on such contracts are

fully recorded in the income statement when they become

known.

Assets held for sale

Assets held for sale include non-current assets (or assets

included in disposal groups) whose carrying amount will be

recovered principally through a sale transaction rather than

through continuing use. Assets held for sale are measured at

the lower of their carrying amount and fair value less disposal

costs.

Employee benefits

Pension plans

Employees of the Group participate in several defined benefit

and/or defined contribution pension plans in accordance with

local conditions and practices in the countries in which the

Group operates. Defined benefit pension plans are based on

the employees’ years of service and the remuneration earned

by the employee during a pre-determined period.

The Group’s obligation to fund defined benefit pension plans

and the annual cost recognised in the income statement is

determined on an actuarial basis using the projected unit credit

method. The portion of net cumulative actuarial gains and

losses which exceeds the greater of 10% of the present value

of the defined benefit obligation and 10% of the fair value of

plan assets at the end of the previous year is amortised over

the average remaining service lives of the employees (the

“corridor approach”). In the context of IFRS First-time

Adoption, the Group elected to recognise all cumulative

actuarial gains and losses that existed at January 1, 2004,

even though it has decided to use the corridor approach for

subsequent actuarial gains and losses. Past service costs are

recognised on a straight-line basis over the average period

remaining until the benefits become vested. The expense

related to the reversal of discounting pension obligations for

defined benefit plans are reported separately as part of the

Fiat Group Consolidated Financial Statements at December 31, 2006 -Notes 100

Group’s financial expense. All other costs relating to

allocations to pension provisions are allocated to costs

by function in the income statement.

The post-employment benefit obligation recognised in the

balance sheet represents the present value of the defined

benefit obligation as adjusted for unrecognised actuarial gains

and losses, arising from the application of the corridor method

and unrecognised past service cost, reduced by the fair value

of plan assets. Any net asset resulting from this calculation is

recognised at the lower of its amount and the total of any

cumulative unrecognised net actuarial losses and past service

cost, and the present value of any economic benefits available

in the form of refunds from the plan or reductions in future

contributions to the plan.

Payments to defined contribution plans are recognised

as an expense in the income statement as incurred.

Post-employment plans other than pensions

The Group provides certain post-employment defined benefit

schemes, mainly healthcare plans. The method of accounting

and the frequency of valuations are similar to those used for

defined benefit pension plans.

The reserve for employee severance indemnities of Italian

companies (“TFR”) is considered a defined benefit plan

and is accounted for accordingly.

Equity compensation plans

The Group provides additional benefits to certain members

of senior management and employees through equity

compensation plans (stock option plans). In accordance

with IFRS 2 – Share-based Payment,these plans represent

acomponent of recipient remuneration. The compensation

expense, corresponding to the fair value of the options at

the grant date, is recognised in the income statement on a

straight-line basis over the period from the grant date to the

vesting date, with the offsetting credit recognised directly in

equity. Any subsequent changes to fair value do not have any

effect on the initial measurement. In accordance with the

transitional provisions of IFRS 2, the Group applied the

Standard to all stock options granted after November 7,

More specifically, vehicles sold with a buy-back commitment

are accounted for as assets in Inventory if the sale originates

from the Fiat Auto business (agreements with normally a

short-term buy-back commitment); and are accounted for in

Property, plant and equipment, if the sale originates from the

Commercial Vehicles business (agreements with normally a

long-term buy-back commitment). The difference between the

carrying value (corresponding to the manufacturing cost) and

the estimated resale value (net of refurbishing costs) at the end

of the buy-back period, is depreciated on a straight-line basis

over the same period. The initial sale price received is

recognised as an advance payment (liability). The difference

between the initial sale price and the buy-back price is

recognised as rental revenue on a straight-line basis over

the term of the operating lease.

Revenues from services and from construction contracts

are recognised by reference to the stage of completion

(the percentage of completion method).

Revenues also include lease rentals and interest income

from financial services companies.

Cost of sales

Cost of sales comprises the cost of manufacturing products

and the acquisition cost of purchased merchandise which has

been sold. It includes all directly attributable material and

production costs and all production overheads. These include

the depreciation of property, plant and equipment and the

amortisation of intangible assets relating to production and

write-downs of inventories. Cost of sales also includes freight

and insurance costs relating to deliveries to dealer agency fee

in the case of direct sales.

Cost of sales also includes provisions made to cover the

estimated cost of product warranties at the time of sale to

dealer networks or to the end customer.Revenues from the

sale of extended warranties and maintenance contracts are

recognised over the period during which the service is

provided.

Expenses which are directly attributable to the financial

services businesses, including the interest expense related to

the financing of financial services businesses as a whole and