Travelers 2003 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2003 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

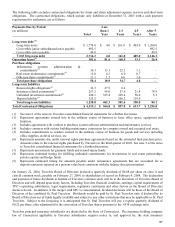

59

Bond achieved significant growth in 2003 in both the surety and executive liability markets. A decrease in capacity in

the surety industry, driven by an increase in claim frequency and severity in accident years 1999 through 2001 for the

surety industry, enabled Bond to increase prices for all surety products. In 2004, Bond expects surety price increases

to moderate compared to 2003 price increases. In the executive liability market for middle and small private accounts

and not-for-profit accounts, Bond’s expanding array of products and recognized local expertise enabled it to further

enhance its product and customer diversification, as well as profit opportunities, while realizing significant price

increases. Bond’s focus remains on selective underwriting, selling its products to customers that provide the greatest

opportunities for profit. Bond is also focused on Travelers efforts to cross-sell its expanding array of products to

existing customers of Commercial Lines and Personal Lines.

In Gulf, rate increases began in most lines of business in 2001 and accelerated significantly in 2002. Rate increases

continued in 2003, but at a slower pace than in 2002. Although specific increases varied by region, industry and

product, improvement was consistent across all product lines, with increases averaging well above loss cost trends.

During 2003, Gulf significantly strengthened its reserve position, due to adverse development from prior accident

years in both residual value and core specialty lines.

There are currently various state and federal legislative and judicial proposals to require asbestos claimants to

demonstrate an asbestos illness. At this time it is not possible to predict the likelihood or timing of such proposals

being enacted or the effect if they are enacted. Travelers ongoing analysis of its asbestos reserves did not assume the

adoption of any asbestos reforms. For information about the outlook with respect to asbestos-related claims and

liabilities see “ – Asbestos Claims and Litigation” and “ – Uncertainty Regarding Adequacy of Asbestos and

Environmental Reserves.”

Personal Lines

Personal Lines strategy is to profitably grow its customer base in the independent agent and additional distribution

channels. The core factors underlying the business are controlling operating expenses, sophisticated pricing

segmentation, providing responsive and fair claim settlement practices and providing an efficient sales platform for our

distributors.

During 2003, the personal auto market continued to increase rates in an effort to obtain profitability targets. These

increases, along with maintaining underwriting discipline and focusing on risk segmentation has made significant

progress towards rate adequacy. Personal Lines automobile rates are expected to increase in 2004, moderating slightly

from 2003 levels.

Personal Lines reported strong property underwriting results in 2003 as market conditions for property insurance

improved in 2003. Significant rate increases were earned and the effects of increased underwriting discipline and

product modification were recognized. Catastrophe losses in the year were above average while non-catastrophe claim

frequencies remained below historical averages. Property rate increases are expected to moderate in 2004 but should

continue to offset increases in loss costs.