Travelers 2003 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2003 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

57

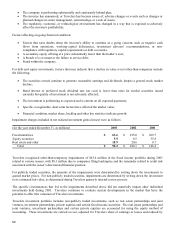

Changes in the general interest rate environment affect the returns available on new investments. While a rising

interest rate environment enhances the returns available on new fixed income investments, it reduces the market value

of existing fixed maturity investments and the availability of gains on disposition. A decline in interest rates reduces

the returns available on new investments, but increases the market value of existing investments and the availability of

realized investment gains on disposition. In 2003, interest rates remained near their lowest levels since the 1950’s.

Consequently, yields available on new investments remain below the existing portfolio’s average book yield. The

continuation of this trend will create downward pressure on the average book yield of fixed income holdings.

As required by various state laws and regulations, Travelers insurance subsidiaries are subject to assessments from

state-administered guaranty associations, second-injury funds and similar associations. In the opinion of Travelers

management, these assessments will not have a material impact on Travelers results of operations.

Some social, economic, political and litigation issues have led to an increased number of legislative and regulatory

proposals aimed at addressing the cost and availability of some types of insurance as well as the claim and coverage

obligations of insurers. While most of these provisions have failed to become law, these initiatives may continue as

legislators and regulators try to respond to public availability, affordability and claim concerns and the resulting laws,

if any, could adversely affect Travelers ability to write business with appropriate returns.

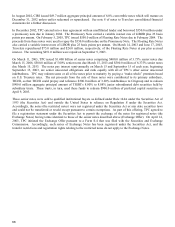

On November 26, 2002, the Terrorism Risk Insurance Act of 2002 (the Terrorism Act) was enacted into Federal law

and established a temporary Federal program in the Department of the Treasury that provides for a system of shared

public and private compensation for insured losses resulting from acts of terrorism committed by or on behalf of a

foreign interest. In order for a loss to be covered under the Terrorism Act (i.e., subject losses), the loss must be the

result of an event that is certified as an act of terrorism by the U.S. Secretary of Treasury. In the case of a war declared

by Congress, only workers’ compensation losses are covered by the Terrorism Act. The Terrorism Insurance Program

(the Program) generally requires that all commercial property/casualty insurers licensed in the U.S. participate in the

Program. The Program became effective upon enactment and terminates on December 31, 2005. The amount of

compensation paid to participating insurers under the Program is 90% of subject losses, after an insurer deductible,

subject to an annual cap. The deductible under the Program was 7% for 2003, and is 10% for 2004 and 15% for 2005.

In each case, the deductible percentage is applied to the insurer’s direct earned premiums from the calendar year

immediately preceding the applicable year. The Program also contains an annual cap that limits the amount of subject

losses to $100 billion aggregate during a program year. Once subject losses have reached the $100 billion aggregate

during a program year, there is no additional reimbursement from the U.S. Treasury and an insurer that has met its

deductible for the program year is not liable for any losses (or portion thereof) that exceed the $100 billion cap.

Travelers deductible under this Federal program is $927.7 million for 2004. Due to the high level of the deductible, in

the opinion of Travelers management, the bill will have little impact on the price or availability of terrorism coverage

in the marketplace. Travelers had no terrorism-related losses in 2003.

While the Terrorism Act provides a Federally-funded “backstop” for commercial property casualty insurers, it also

requires that insurers immediately begin offering coverage for insured losses caused by acts of terrorism. The majority

of Travelers Commercial Lines policies already included such coverage, although exclusions were added to higher-risk

policyholders after September 11, 2001. For those risks considered higher-risk, such as landmark buildings or high

concentrations of employees in one location, Travelers will continue to either decline to offer a renewal or will offer

coverage for losses caused by acts of terrorism on a limited basis, with an explicit charge for the coverage.