Travelers 2003 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2003 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

103

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued

Nature of Operations

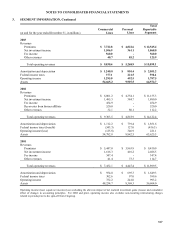

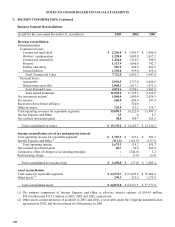

Travelers comprises two business segments: Commercial Lines and Personal Lines.

Commercial Lines

Commercial Lines offers a broad array of property and casualty insurance and insurance-related services.

Protection is afforded to customers of Commercial Lines for the risks of property loss such as fire and

windstorm, financial loss such as business interruption from property damage, liability claims arising from

operations and workers’ compensation benefits through insurance products where risk is transferred from the

customer to Commercial Lines. Coverages include workers’ compensation, general liability, commercial multi-

peril, commercial automobile, property, fidelity and surety, professional liability, and several miscellaneous

coverages.

Commercial Lines is organized into five marketing and underwriting groups, each of which focuses on a

particular client base or product grouping to provide products and services that specifically address customers’

needs. The Core marketing and underwriting groups include National Accounts, Commercial Accounts and

Select Accounts, and Specialty includes Bond and Gulf.

National Accounts provides casualty products to large companies, with particular emphasis on workers’

compensation, general liability and automobile liability. Products are marketed through national and regional

brokers. Programs offered by National Accounts include risk management services, such as claims settlement,

loss control and risk management information services, which are generally offered in connection with a large

deductible or self-insured program, and risk transfer, which is typically provided through a guaranteed cost or

retrospectively rated insurance policy. National Accounts also includes Travelers residual market business,

which primarily offers workers’ compensation products and services to the involuntary market.

Commercial Accounts serves primarily mid-sized businesses for casualty products and large, mid-sized and

small businesses for property products. Commercial Accounts sells a broad range of property and casualty

insurance products, with an emphasis on guaranteed cost products, through a large network of independent

agents and brokers. Within Commercial Accounts Travelers has a specialty unit which primarily writes

coverages for the transportation industry and has dedicated operations that exclusively target the construction

industry, providing insurance and risk management services for virtually all areas of construction. These

dedicated operations reflect Travelers focus on industry specialization.

Select Accounts serves small businesses. Select Accounts’ products are generally guaranteed cost policies, often

a packaged product covering property and liability exposures. The products are sold through independent

agents.

Bond markets its products to national, mid-sized and small customers as well as individuals, and distributes them

through both national and wholesale brokers, and retail agents and regional brokers. Bond’s range of products

includes fidelity and surety bonds, directors’ and officers’ liability insurance, errors and omissions insurance,

professional liability insurance, employment practices liability insurance, fiduciary liability insurance, and other

related coverages.

Gulf markets products to national, mid-sized and small customers, and distributes them through both wholesale

brokers and retail agents. Gulf provides a broad range of specialty coverages, including management and

professional liability, excess and surplus lines, environmental, umbrella and fidelity. Gulf also provides

insurance products specifically designed for financial institutions, the entertainment industry and sports

organizations.