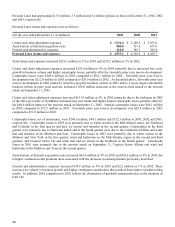

Travelers 2003 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2003 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

58

Commercial Lines

In 2003, the trend of higher rates continued in Commercial Lines, although at a moderated level over 2002, and some

of the increases varied significantly by region, business segment and line of business. These increases were necessary

to offset the impact of rising loss cost trends, reduction in investment yields and the decline in profitability from the

competitive pressures of the last decade. Since the terrorist attack on September 11, 2001, there has been greater

concern over the availability, terms and conditions, and pricing of reinsurance. As a result, the primary insurance

market is expected to continue to see rate increases, although at moderated levels from the past two years, and

continued restrictive terms and conditions for certain coverages where adequate pricing cannot be achieved.

In National Accounts, where programs include risk management services, such as claims settlement, loss control and

risk management information services, generally offered in connection with a large deductible or self-insured program,

and risk transfer, typically provided through a retrospectively rated or guaranteed cost insurance policy, new business

levels increased in 2003 due to a significant renewal rights transaction and to a reduction in the number of competitors

in the marketplace. Customer retention has remained consistent with prior periods. Travelers has benefited from

higher rates and believes that pricing will continue to stay firm into 2004. However, Travelers will still continue to

selectively reject business that is not expected to produce acceptable returns. Travelers anticipates that the premium

and fee income growth experienced in 2003 will continue into 2004. Included in National Accounts is service fee

income for policy and claim administration of various states’ Workers’ Compensation Residual Market pools. After

several years of depopulation, these pools began to repopulate in 2000 and grow significantly. Premium that Travelers

services for these pools grew 24% in 2003 and is expected to modestly grow in 2004.

Commercial Accounts achieved price increases on renewal business of 10%, 22% and 19% during 2003, 2002 and

2001, respectively, improving the overall profit margin in this business, more than offsetting the impacts of rising loss

cost, reinsurance costs and lower investment yields. The 2003 price increases began moderating compared to the 2002

price increases. New business levels also increased during 2003 across most products where Commercial Accounts

benefited from Travelers underwriting specialization, financial strength and limits capacity. In 2004, Travelers will

continue to seek increased new business levels on products producing acceptable returns, higher retention rates on its

existing business and overall rate increases, although the rate of increase may vary by line of business and, on an

overall basis, may moderate compared to 2003.

Also in Commercial Accounts, during 2002 the operations of American Equity and Associates were determined to be

non-strategic. Accordingly, these operations were placed in run-off during the first and fourth quarters of 2002,

respectively, which included non-renewals of inforce policies and a cessation of writing new business, where allowed

by law. These operations were acquired in the fourth quarter of 2001 from Citigroup as part of the Northland and

Associates acquisitions previously discussed. Net written premium for these combined operations was $1.0 million

and $86.8 million in 2003 and 2002, respectively.

Select Accounts also achieved price increases on renewal business of 14%, 17% and 14% in 2003, 2002 and 2001,

respectively, improving the overall profit margin in this business, more than offsetting the impact of rising loss cost

and lower investment yields. Price increases varied significantly by region, industry and product. However, the ability

of Select Accounts to achieve future rate increases is subject to regulatory constraints in some jurisdictions. Select will

continue to seek rate increases in 2004, but the amount of increase may continue to decline as compared to the past

year. Customer retention levels increased in 2003 over 2002 and loss cost trends in Select Accounts remained stable

due to Travelers continued disciplined approach to underwriting and risk selection. Travelers will continue to pursue

business based on Travelers ability to achieve acceptable returns.