Travelers 2003 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2003 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

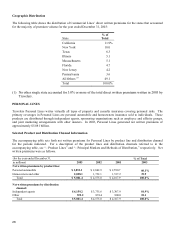

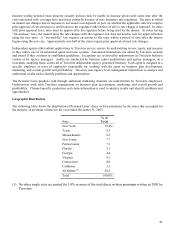

30

Personal Lines also markets through additional distribution channels, including sponsoring organizations such as

employers and consumer associations, and joint marketing arrangements with other insurers. Travelers handles the

sales and service for these programs either through a sponsoring independent agent or through two of Travelers call

center locations. Travelers is one of the leading providers of personal lines products to members of affinity groups. A

number of well-known corporations endorse Travelers product offerings to their employees primarily through a payroll

deduction payment process. Travelers has significant relationships with the majority of the American Automobile

Association (AAA) clubs in the United States and other affinity groups that endorse Travelers tailored offerings to

their members. Since 1995, Travelers has had a marketing agreement with GEICO to receive referrals for

homeowners business. This agreement has added profitable business and helped to geographically diversify the

homeowners line of business.

Pricing and Underwriting

Pricing levels for Personal Lines property and casualty insurance products are generally developed based upon the

frequency and severity of incurred losses and loss adjustment expense, the expenses of producing business and a

reasonable allowance for profit and contingencies. Travelers has a disciplined approach to underwriting and risk

management that places emphasis on underwriting profit rather than market share.

Travelers has developed a product management methodology that integrates the disciplines of underwriting, claim,

actuarial and product development. This approach is designed to maintain high quality underwriting discipline and

pricing segmentation. Proprietary data is analyzed with respect to Travelers Personal Lines business over many years.

Travelers uses a variety of proprietary and vendor produced risk differentiation models to facilitate its pricing

segmentation. Travelers Personal Lines product managers establish strict underwriting guidelines integrated with its

filed pricing and rating plans, which enable Travelers to streamline its risk selection and pricing processes.

Pricing for personal automobile insurance is driven by changes in the frequency of claims and by inflation in the cost

of automobile repairs, medical care and litigation of liability claims. As a result, the profitability of the business is

largely dependent on promptly identifying and rectifying disparities between premium levels and projected claim

costs, and obtaining approval from state regulatory authorities when necessary for filed rate changes.

Pricing in the homeowners business is also driven by changes in the frequency of claims and by inflation in the cost of

building supplies, labor and household possessions. Most homeowners policies offer, but do not require, automatic

increases in coverage to reflect growth in replacement costs and property values. In addition to the normal risks

associated with any multiple peril coverage, the profitability and pricing of homeowners insurance is affected by the

incidence of natural disasters, particularly hurricanes, winter storms, wind and hail, water damage, earthquakes and

tornadoes. In order to reduce Travelers exposure to catastrophe losses, Travelers has limited the writing of new

homeowners business and selectively non-renewed existing homeowners business in some markets. In addition,

underwriting standards have been tightened, price increases have been implemented in some catastrophe-prone areas,

and deductibles have been put in place in hurricane and wind and hail prone areas. Travelers uses computer-modeling

techniques to assess its level of exposure to loss in hurricane and earthquake catastrophe-prone areas. Changes to

methods of marketing and underwriting in some jurisdictions are subject to state-imposed restrictions, which can make

it more difficult for an insurer to significantly reduce catastrophe exposures.