Reebok 2008 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2008 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220

|

|

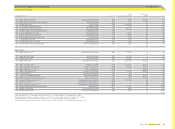

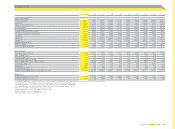

adidas Group Annual Report 2008 213

Segmental reporting Information regarding the fi nancial position and results of operations

in individual brands (segments) and regions. This gives an indication of developments in the

individual segments and their contribution to the Group’s results.

Sell-through An indicator of how fast retailers are selling a particular product to the

consumer.

Shareholder value A management concept that focuses strategic and operational decision-

making on steadily increasing a company’s value for shareholders.

Shop-in-shop adidas, Reebok or Rockport area within a larger store. The concept may be

operated by the store or the adidas Group depending on individual arrangements. The goal of

this distribution method is to give consumers a similar experience to an own-retail environment,

albeit on a smaller scale.

Signature collection Product collection which carries the name and /or visuals relating to a

top athlete.

Sourcing Process of managing external suppliers in order to commercialise, produce and

deliver fi nal products to customers.

Sporting goods channel Sports retail store, offering a very broad product range, which usually

covers apparel, footwear and hardware in a wide range of sports categories. Compared to sport

specialty shops, stores are bigger with approx. 40,000 to 50,000 square feet.

Sport specialty Retail shop, specialising in sports products only and offering a very deep

product range (often in a limited number of sports categories) rather than a broad one. The size

of these shops is typically about 2,500 to 10,000 square feet.

Stakeholders All parties that have a direct or indirect interest in a company’s performance

and results. For the adidas Group, this includes credit providers, shareholders, consumers,

retailers, distributors, licensees, supply chain business partners, employees, international

sports bodies, non-governmental organisations, the media, etc.

Supply chain Refers to the system and organisation from product sourcing through to end

customer delivery.

Swaps A derivative in which two counterparties agree to exchange one stream of cash fl ows

against another stream.

Synergies Additional savings or revenue growth when one combined enterprise is created

from two or more separate parts.

Tax rate Indicates the tax rate paid by a company. Calculated by dividing taxes by income

before taxes.

Top-down, bottom-up Specifi c concept for information and knowledge processing. Information

and empowerment of management decisions is delegated from top to bottom in a fi rst step.

After going into more detail on the bottom level, the fi nal information /decision is transported

back to the top.

VOC (Volatile Organic Compounds) Solvents that can cause breathing and health problems.

VOCs are by-products of the shoe manufacturing process. Due to health concerns, the adidas

Group has set a clear goal to steadily reduce the usage of these compounds in the production

process.

Weighted average cost of capital Calculation of the cost of capital according to the debt /equity

structure, utilising a weighted average cost of capital (WACC) formula. The cost of equity is typi-

cally computed utilising a risk-free rate, market risk premium and a beta factor. The cost of debt

is calculated through the risk-free rate, credit spread and average tax rate see also Beta Factor

and Market Risk Premium.

Working capital A company’s short-term disposable capital used to fi nance the day-to-day

operations.

Working capital = total current assets – total current liabilities.

see also Operating Working Capital

Working capital turnover Shows how often a working capital item was used in and replaced by

the generation of sales in the period under review. The ratio shows how long working capital is

tied up and thus is an indicator of the volume of capital needed to generate sales. The higher the

ratio, the more positive it is deemed to be.

Working capital turnover = net sales / working capital.