Reebok 2008 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2008 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

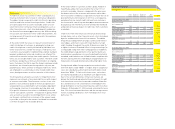

112 Group Management Report – Our Financial Year Risk and Opportunity Report

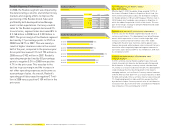

Risks from rising input costs

Raw material and labour costs account for approximately 70%

of the Group’s cost of sales. Prices of materials such as rub-

ber, and those which closely correlate with the oil price, are

especially subject to the risk of price changes. As our order-

ing process and price negotiations usually take place around

six months in advance of production, our sourcing function

has visibility and reaction time to manage and plan for sharp

increases in input costs.

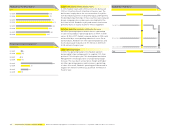

To reduce the fi nancial impact on our product margins from

higher sourcing costs, we are implementing further lean

manufacturing techniques at our partner factories, eliminating

time and cost from the procurement process, re-engineering

our products where possible, and selectively increasing prices

if necessary see Global Operations, p. 064. In addition, in the

medium term we have the ability to adapt our sourcing struc-

ture to take advantage of more competitive pricing in other

locations.

During 2008, raw material price volatility, including record oil

prices, and the increase in labour costs in Asia negatively

impacted our sourcing terms negotiated for 2009 production.

As we begin planning for 2010, although raw material pricing

has eased for the time being, renewed increase in volatility

cannot be ruled out given the current macro economic uncer-

tainty. Therefore, we continue to assess the medium-term risks

from rising input costs as having a medium likelihood and a

medium potential fi nancial impact.

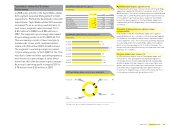

Supplier default risks

Over 95% of our product offering is sourced through indepen-

dent suppliers mainly located in Asia see Global Operations,

p. 064. To reduce the risk of business interruptions following a

potential supplier default, we work with vendors who demon-

strate reliability, quality, innovation and continuous improve-

ment. In addition, we have bought insurance coverage for the

risk of business interruptions caused by physical damage to

supplier premises. In 2008, the Group has again signifi cantly

reduced the number of independent manufacturers through

the further rationalisation of our supplier organisation see

Global Operations, p. 064. This exercise has allowed us to reduce

risk by simplifying our sourcing structure and focusing on the

highest-quality suppliers, without compromising our fl exibility

or competitiveness.

Therefore, we continue to assess supplier risks as having a low

likelihood of occurrence and potential fi nancial impact.

Product quality risks

The adidas Group faces a risk of selling defective products,

which may result in injury to consumers and /or image impair-

ment. We mitigate this risk through rigorous testing prior to

production, close cooperation with suppliers throughout the

manufacturing process, random testing after retail delivery,

open communication about defective products and quick

settlement of product liability claims when necessary. In

2008, we recalled 1,000 CCM Hockey and Reebok Hockey

helmets manufactured in Canada. The helmet’s chinstrap

could unexpectedly disengage while in use, posing a head

and neck injury risk to consumers when the helmet falls.

No injury was reported.

Our assessment of product quality risk remains unchanged

versus the prior year. We regard the likelihood of signifi cant

product liability cases or having to conduct wide-scale product

recalls as low. As we have insurance protecting us against the

fi nancial consequences of signifi cant product liability cases, we

also assess the fi nancial impact as low.

Customer risks

Customer risks arise from our dependence on key customers

who have the ability to exert bargaining power and can there-

fore cause considerable margin pressure or cancel orders.

These risks exist not only due to the relative size of some of our

major customers, but also as a result of our limited ability to

infl uence how they conduct business and the external impacts

of the consumer environment in which they operate.

To limit these risks, we utilise a broad distribution strategy

which includes expanding our controlled space activities. This

enables us to reduce negative consequences resulting from

sales shortfalls that can occur with key customers. Specifi -

cally, no customer at adidas, Reebok and TaylorMade-adidas

Golf accounted for more than 10% of brand sales in 2008.

When necessary, we restrict or limit the distribution of our

brands to protect brand image or product margins, and to

streamline supply. In 2008, we continued our retail segmenta-

tion strategy. By segmenting product offer to our customers,

we limit the risk of increased competition which can result

in higher sales discounts. For example, in the course of 2008,

the Group decided to limit the Reebok product offering to an

important mall-based key account in North America.

Due to the challenging economic situation and diffi culties at

some major sporting goods retailers in developed markets,

we continue to view the risk of a strong reduction of business

with one of our brands’ biggest retailers as having a medium

likelihood of occurrence. Such an event could have a medium

fi nancial impact on the sales and profi tability of a particular

region. On a Group level, given the deterioration in several

markets compared to the prior year, we now view the fi nancial

impact from customer risks as medium.