Chrysler 2009 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2009 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

|

|

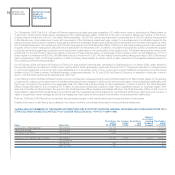

87

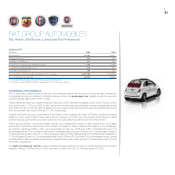

FIAT GROUP AUTOMOBILES

Fiat, Abarth, Alfa Romeo, Lancia and Fiat Professional

HIGHLIGHTS

(E million) 2009 2008

Net revenues 26,293 26,937

Trading profit/(loss) 470 691

Operating profit/(loss) (*) 217 460

Investments in tangible and intangible assets 1,495 2,288

of which capitalised R&D costs 446 641

Total R&D expenditure (**) 669 843

Cars and light commercial vehicles delivered (no. of units) 2,150,700 2,152,500

No. of employees at year end 54,038 52,634

(*) Including restructuring costs and other unusual income/(expense).

(**) Includes capitalised R&D and R&D charged directly to the income statement.

COMMERCIAL PERFORMANCE

After a particularly negative start to the year, the scrapping incentives introduced in several major markets led

to a gradual recovery in demand in Western Europe, where the passenger car market closed the year with

volumes slightly higher than 2008 (+0.5%).

These incentives had a very positive impact in Germany, where demand increased 23.2%, and in France, where

the market grew 10.7% over 2008. In Italy, government incentives helped maintain demand substantially in line

with 2008 (-0.2%). In both the UK and Spain, however, where incentives were introduced towards the end of the

first half, demand was down 6.4% and 17.9%, respectively.

Outside of Western Europe, performance in the Sector’s key markets was mixed. In Poland, demand remained

stable (+0.1%), while in Brazil there was a further increase (+12.6%) over the positive performance in 2008

underpinned by government purchase incentives and a generally favourable economic environment.

FGA’s strong offering of environmentally-friendly cars enabled the Sector to fully benefit from eco-based

government incentives. Fiat Group Automobiles continued to make positive share gains in the passenger

car market, reaching 32.8% in Italy (+0.9 percentage points over 2008) and 8.8% in Western Europe (+0.6

percentage points). FGA’s relative performance was particularly strong in Germany (+1.5 percentage points to

4.7%) and positive also in the UK (+0.6 percentage points to 3.5%). Market share for the Fiat brand increased to

7.1% in Western Europe (+0.5 percentage points over 2008) and 25.5% in Italy (+0.4 percentage points). Lancia

and Alfa Romeo also increased market share in Western European, each gaining 0.1 percentage points to 0.9%

and 0.8%, respectively.

The light commercial vehicle market in Western Europe declined 27.4% over 2008. Demand fell in all major

markets: France (-18.8%), Italy (-21.4%), Germany (-24.8%), the UK (-35.5%) and Spain (-35.6%).