Chrysler 2009 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2009 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

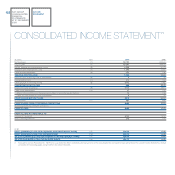

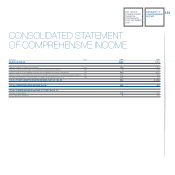

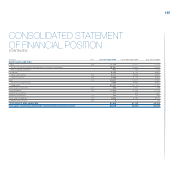

|

|

115

PRODUCTION SYSTEMS

Comau

HIGHLIGHTS

(E million) 2009 2008

Net revenues 728 1,123

Trading profit/(loss) (28) 21

Operating profit/(loss) (*) (32) -

Investments in tangible and intangible assets 13 17

of which capitalised R&D costs 2 3

Total R&D expenditure (**) 10 13

No. of employees at year end 11,708 11,445

(*) Including restructuring costs and other unusual income/(expense).

(**) Includes capitalised R&D and R&D charged directly to the income statement.

OPERATING PERFORMANCE

In 2009, the Sector’s reference market was negatively impacted by the global financial and industrial crisis which

affected all markets.

In the western hemisphere, all automakers reduced capital investment to minimum levels and new model launches

were scaled back or delayed.

Cuts in capital investment were less severe in Mercosur and China however, with limited new investment commitments

in the first half of the year but a recovery in the second half.

Service activities, by contrast, saw an increase in Mercosur countries.

Additionally, the tendency to favour conversion and rationalisation of existing production capacity, rather than the

construction of new plants, continued.

In the last quarter, some improvement was observed in North America following the conclusion of bankruptcy

proceedings for Chrysler and General Motors.

Comau’s plan to restructure and redefine the scope of its activities and geographic presence, initiated in prior years in

response to difficult market conditions, together with a series of temporary cost-cutting measures, made it possible

to limit losses from significantly lower business volumes.

In 2009, Comau sold its companies in South Africa and the German company germanINTEC (engineering

activities).

New orders for contract work, totalling €528 million, were 38% lower than in 2008 (-36% on a like-for-like basis).

Overall, 27% of new contract orders were acquired in Europe and 47% in the NAFTA region, with the remaining

26% in the Mercosur region and emerging markets. By customer, 20% of orders were received from Fiat Group

companies and 80% from other automakers. At 31 December 2009, the order backlog totalled €478 million, a 9%

decrease over the previous year.

Services benefited from growth in Mercosur, which did not however offset the contraction in orders in Europe resulting

from the redefinition of the scope of activities.