Chrysler 2009 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2009 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

|

|

REPORT ON

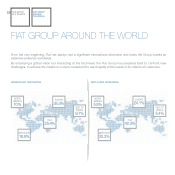

OPERATIONS

SHAREHOLDERS

32

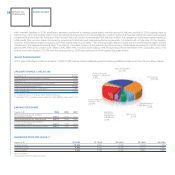

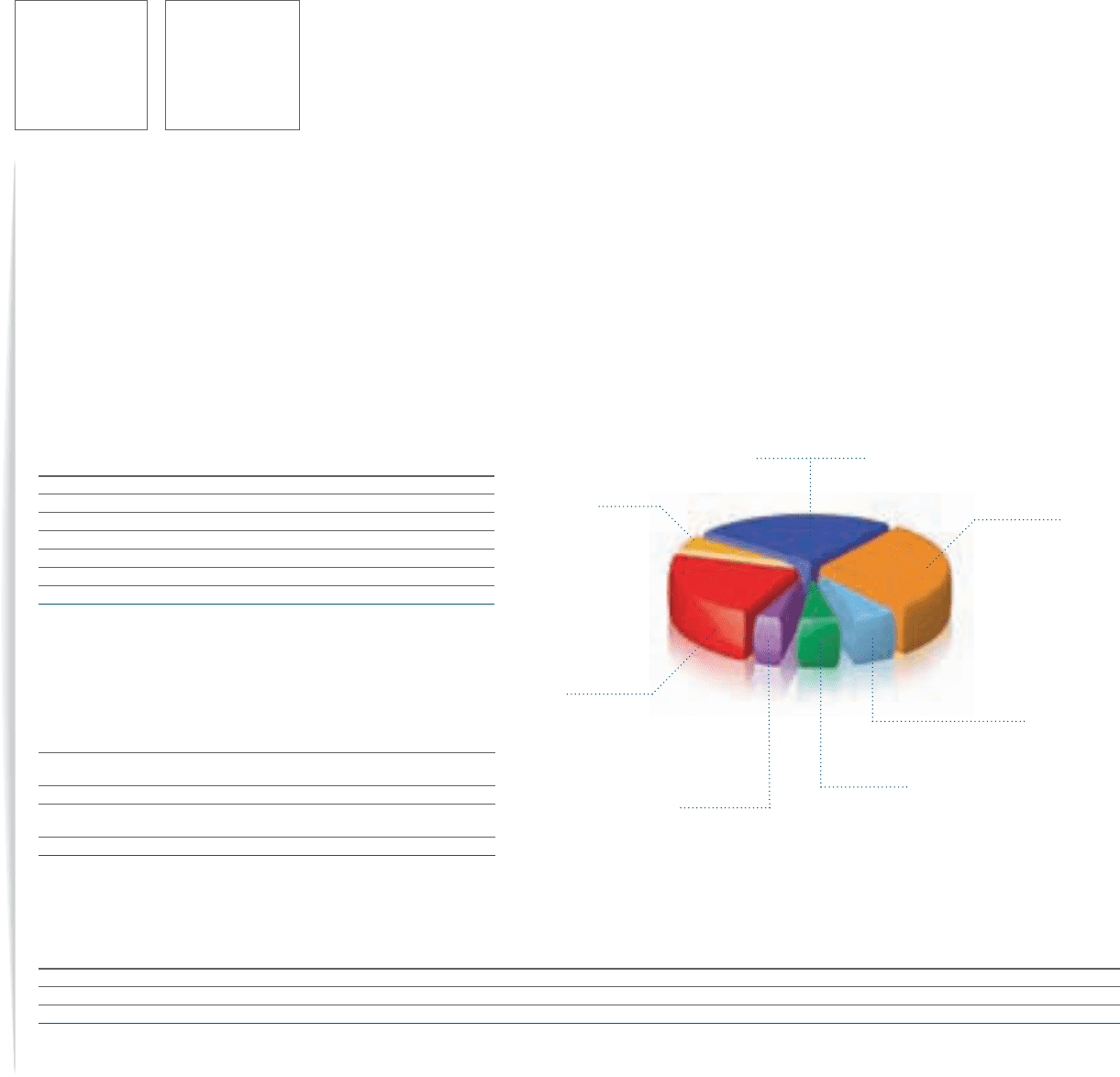

Exor S.p.A.(*)

30.5%

Capital Research

& Management Co.

5.2%

FMR LLC (**)

5.0%

Other shareholders

25.4%

Other institutional

investors - outside EU

4.8%

Other institutional

investors - EU

22.6%

BlackRock

Investment

Management

(UK) Limited

3.0%

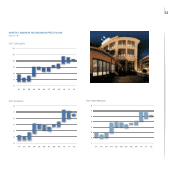

After dramatic declines in 2008, pessimistic sentiment continued to depress global equity markets during the first two months of 2009 pushing them to

historic lows. Hit by the liquidity crisis in the international banking system, and several failures, investors feared that financial institutions which had received

considerable government aid to support them through the crisis could be nationalised. But financial markets then staged an unexpected uptick based on

initial results from recovery plans introduced by governments and improved business performance generally. Confidence did not fully return to the markets,

however, and investors looked forward to 2010 with a great deal of uncertainty. Fear of a large-scale default in Dubai at the end of November again created

turbulence in the markets for several days. The majority of markets closed out the year with a partial recovery of the losses experienced in 2008: Frankfurt

gained 24%, Paris 22%, London 22%, Madrid 30%, Milan 19%, the Dow Jones was up 19%, Hong Kong 52% and the Nikkei 19%. During this period, Fiat

shares more than doubled (+123%) over the closing price for 2008 (best performer in 2009 against European peers).

MAJOR SHAREHOLDERS

At the date of this Report, Fiat had a total of 1,092,247,485 ordinary shares outstanding and the following institutions held more than 2% of ordinary shares:

(figures in E) 31.12.09 31.12.08 28.12.07 29.12.06 30.12.05

Ordinary shares 10.250 4.590 17.695 14.468 7.360

Preference shares 6.000 2.440 14.640 12.119 5.930

Savings shares 6.295 3.035 14.655 13.880 6.584

(Source: Reuters)

(*) Equivalent to the closing auction price.

(figures in E) 2009 2008 2007

Basic earnings/(loss) per ordinary

and preference share (0.677) 1.290 1.537

Basic earnings/(loss) per savings share (0.677) 1.445 1.692

Diluted earnings/(loss) per ordinary

and preference share (0.677) 1.285 1.526

Diluted earnings/(loss) per savings share (0.677) 1.440 1.681

Exor S.p.A. (*) 30.5%

Capital Research & Management Company 5.2%

FMR LLC (**) 5.0%

BlackRock Investment Management (UK) Limited 3.0%

Other institutional investors - EU 22.6%

Other institutional investors - outside EU 4.8%

Other shareholders 25.4%

(*) In addition to 3.5% of ordinary shares held by Fiat S.p.A.

(**) Including 1.75% of ordinary shares in relation to which FMR has sole power to vote.

REFERENCE PRICE PER SHARE (*):

EARNINGS PER SHARE

ORDINARY SHARES: 1,092,247,485