Chrysler 2009 Annual Report Download - page 225

Download and view the complete annual report

Please find page 225 of the 2009 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

|

|

224 FIAT GROUP

CONSOLIDATED

FINANCIAL

STATEMENTS

AT 31 DECEMBER

2009

NOTES

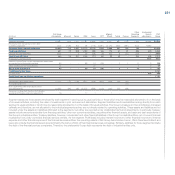

The quantitative data reported in the following do not have any value of a prospective nature, in particular the sensitivity analysis on market risks, is unable

to reflect the complexity of the market and its related reaction which may result from every change which may occur.

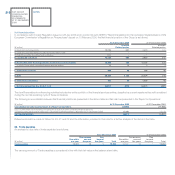

Credit risk

The maximum credit risk to which the Group is theoretically exposed at 31 December 2009 is represented by the carrying amounts stated for financial

assets in the statement of financial position and the nominal value of the guarantees provided on liabilities or commitments to third parties as discussed in

Note 30.

Dealers and final customers are subject to specific assessments of their creditworthiness under a detailed scoring system; in addition to carrying out this

screening process, the Group also obtains financial and non-financial guarantees for risks arising form to credit granted for the sale of cars, commercial

vehicles and Agricultural and Construction equipment. These guarantees are further strengthened where possible by reserve of title clauses on financed

vehicle sales to the sales network and on vehicles assigned under finance leasing agreements.

Balances which are objectively uncollectible either in part or for the whole amount are written down on a specific basis if they are individually significant. The

amount of the write-down takes into account an estimate of the recoverable cash flows and the date of receipt, the costs of recovery and the fair value of any

guarantees received. Impairment losses are recognised for receivables which are not written down on a specific basis, determined on the basis of historical

experience and statistical information.

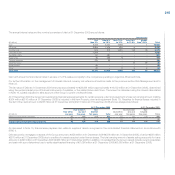

Out of Receivables for financing activities amounting to €12,695 million at 31 December 2009 (€13,136 million at 31 December 2008), balances

totalling €60 million (€82 million at 31 December 2008) have been written down on an individual basis. Of the remainder, balances totalling €426 million

(€263 million at 31 December 2008) are past due up to one month, while balances totalling €918 million are past due by more than one month (€413 million

at 31 December 2008). In the event of instalment payments, even if only one instalment is overdue, the whole amount of the receivable is classified as such.

Out of Trade receivables and Other receivables totalling €6,178 million at 31 December 2009 (€6,763 million at 31 December 2008), balances totalling

€67 million (€101 million at 31 December 2008) have been written down on an individual basis. Of the remainder, balances totalling €280 million (€363 million

at 31 December 2008) are past due up to one month, while balances totalling €568 million (€615 million at 31 December 2008) are past due by more than

one month.

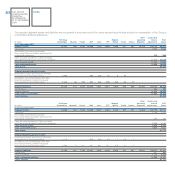

The significant increase in the past due component in receivables from financing activities is mainly attributable to the performance of subsidised loans

granted by Banco CNH Capital S.A. as part of the development/subsidised loans program for agriculture of the Brazilian development agency managed

through Banco Nacional de Desenvolvimento Economico e Social (“BNDES”). The increase in the past due portion of these receivables is due to the general

debt relief programs that were implemented from time to time by the Brazilian government between 2005 and 2009 to support an agricultural industry going

through a difficult period by extending the credit terms on outstanding loans. The Group has recognised as past due receivables those balances for which

the minimum payments required under the debt relief program have not been respected. Total rescheduled outstanding loans amounted to approximately

2 billion Reais (approximately €0.8 billion) at 31 December 2009; Banco CNH Capital had a net overdue balance with its customers of approximately

1.1 billion Reais (approximately €0.4 billion). In order to deal with an increasing credit risk, mitigated however by the fact that it has reservation of title on

the assets to which its lending relates, the Brazilian company adjusted the level of its allowances in 2009. In the meantime the BNDES has continued its

financial support for the company and the subsidised loan programs.

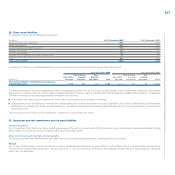

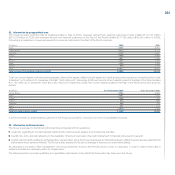

Liquidity risk

Liquidity risk arises if the Group is unable to obtain under economic conditions the funds needed to carry out its operations.

The two main factors that determine the Group’s liquidity situation are on one side the funds generated by or used in operating and investing activities and

on the other the debt lending period and its renewal features or the liquidity of the funds employed and market terms and conditions.

As described in the Risk management section, the Group has adopted a series of policies and procedures whose purpose is to optimise the management

of funds and to reduce the liquidity risk, as follows:

centralising the management of receipts and payments, where it may be economical in the context of the local civil, currency and fiscal regulations of the

countries in which the Group is present;

maintaining an adequate level of available liquidity;

diversifying the means by which funds are obtained and maintaining a continuous and active presence on the capital markets;