Chrysler 2009 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2009 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

|

|

146 FIAT GROUP

CONSOLIDATED

FINANCIAL

STATEMENTS

AT 31 DECEMBER

2009

NOTES

expenditures, incurs borrowing costs or undertakes activities that are necessary to prepare the asset for its intended use or sale

from 1 January 2009. No significant accounting effects arose in 2009 from adopting the revised standard.

Amendment to IFRS 2 – Share-based Payment: Vesting Conditions and Cancellations

The amendment to IFRS 2 - Share-based Payment: Vesting Conditions and Cancellations clarifies that for the purpose of

measuring share-based payments, only service conditions and performance conditions may be considered vesting conditions.

Any other clauses shall be considered non-vesting conditions and included in the determination of fair value at the grant

date. The amendment also specifies that all cancellations, whether by the entity or by other parties, should receive the same

accounting treatment.

The Group retrospectively adopted the amendment from 1 January 2009; no effects arose from first-time adoption because the

share-based payments outstanding within the Group and not fully vested do not provide for vesting conditions different from

performance conditions and service conditions as defined by the amendment and because no awards were cancelled during

the period.

Improvement to IAS 16 – Property, Plant and Equipment

The improvement to IAS 16 – Property, Plant and Equipment requires an entity that in the course of its ordinary activities routinely

sells items of property, plant and equipment that it has held for rental to others, to transfer such assets to inventories when they

cease to be rented and become held for sale. As a consequence, the proceeds from the sale of such assets shall be recognised

as revenue. Payments made to manufacture or acquire assets held for rental to others or those received from the subsequent

sale of such assets are considered to arise from operating activities for the purposes of the Statement of cash flows.

Until 31 December 2008 the Group classified as Inventories leased assets that ceased to be rented under operating leases

and were held for sale. When these assets were sold on a final basis, however, the Group recognised any gains or losses

on disposal as Other income (expenses). Additionally, in the Statement of cash flows the Group classified cash flows arising

from the manufacture, acquisition or disposal of the assets held for rental under operating leases as cash flows from (used in)

investment activities. The Group also followed the accounting treatment used for leased assets for assets of the Trucks and

Commercial Vehicles Sector sold under a buy-back commitment; at the end of the buy-back agreement term, however, these

assets remained classified as Property, plant and equipment and any gains or losses on disposal were recognised as Other

income (expenses). Cash flows arising from these assets were classified as cash flows from (used in) operating activities in the

Statement of cash flows.

The Group adopted the amendment to IAS 16 retrospectively on 1 January 2009. As the method of measuring leased assets

and assets sold under buy-back commitments was the same as that used for measuring inventory, the application of the new

accounting treatment did not lead to any effect on Equity at 1 January 2008 or 31 December 2008, and on the Profit of 2008.

Applying the amendment did however require certain items in the Statement of financial positions at 1 January 2008 and

31 December 2008 to be reclassified and certain items in the Income statement for 2008 and the Statement of cash flows for

2008 presented as comparative to be recalculated.

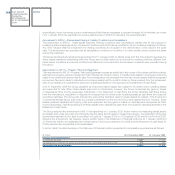

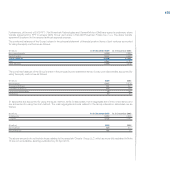

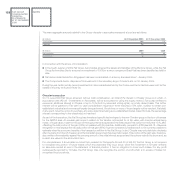

In further detail, the effects arising on the Statement of financial position presented for comparative purposes are as follows:

(€ million) At 31 December 2008 At 1 January 2008

Property, plant and equipment

As previously reported 12,607 11,246

Reclassification to Inventory for assets sold under buy-back commitments and held for sale (92) (34)

Amount after the reclassification 12,515 11,212