SunTrust 2007 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2007 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

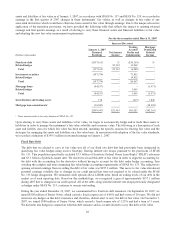

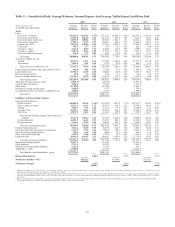

Available for Sale and Trading Securities

The available for sale debt securities that were transferred to trading were substantially all of the debt securities within

specific asset classes, whether the securities were valued at an unrealized loss or unrealized gain. We elected to

reclassify approximately $15.4 billion of securities to trading at January 1, 2007, as well as an additional $600 million

of purchases of similar assets that occurred during the first quarter of 2007. The reduction to opening retained earnings

related to reclassifying the $15.4 billion of securities to trading was $147.4 million. This net unrealized loss was already

reflected in accumulated other comprehensive income and, therefore, upon reclassification to retained earnings, there

was no net impact to total shareholders’ equity. Our securities portfolio is generally of high credit quality, such that the

opening retained earnings adjustment was not significantly impacted by the credit risk embedded in the assets, but rather

due to interest rates.

We elected to move these available for sale securities to trading securities in order to initially seed the trading securities

portfolio that we intended to actively manage in connection with the overall management of our balance sheet. The

transfer of securities to trading enabled us to more actively trade a more significant portion of our investment portfolio

and reduce the overall size of the available for sale portfolio. In determining the assets to be sold, we considered

economic factors, such as yield, collateral, interest terms, capital efficiency, and duration, in relation to our balance

sheet strategies. In evaluating our total available for sale portfolio of approximately $23 billion at January 1, 2007, we

determined that approximately $3 billion of securities were not available or were not practicable to be fair valued and

reclassified to trading under SFAS No. 159, as these securities had matured or been called during the quarter, were

subject to business restrictions, were privately placed or had nominal principal amounts. Approximately $5 billion of

securities aligned with our recent balance sheet strategy, due to the nature of the assets (such as 30-year fixed rate

mortgage backed securities (“MBS”), 10/1 adjustable rate mortgages (“ARMs”), floating rate asset backed securities

(“ABS”) and municipal bonds); therefore, the securities continued to be classified as available for sale. These securities

yielded over 5.6%, had a duration over 4.0%, and were in a $6.7 million net unrealized gain position as of January 1,

2007. The remaining $15.4 billion of securities, which included hybrid ARMs, commercial MBS, collateralized

mortgage obligations (“CMO”) and MBS (excluding those classes of MBS that remained classified as securities

available for sale), yielded approximately 4.5% and had a duration under 3.0%. The approximate $600 million of

securities that were purchased in the first quarter and originally classified as available for sale were similar to the

securities reclassified to trading on January 1, 2007 upon adoption of SFAS No. 159; accordingly, we reclassified these

securities to trading pursuant to the provisions of SFAS No. 159.

During the first quarter of 2007, in connection with our decision to early adopt SFAS No. 159, we purchased

approximately $1.7 billion of treasury bills, which were classified as trading securities, and approximately $3.2 billion

of 30-year fixed rate MBS, which were classified as securities available for sale. We entered into approximately $13.5

billion notional of interest rate derivatives to mitigate the fair value volatility of the available for sale securities that had

been reclassified to trading. Finally, as part of our asset/liability strategies, we executed an additional $7.5 billion

notional receive-fixed interest rate swaps that were designated as cash flow hedges under SFAS No. 133 on floating rate

commercial loans.

During the second quarter of 2007, we sold substantially all of the $16.0 billion in securities transferred to trading at

prices that, in the aggregate and including the hedging gains and losses, approximated the fair value of the securities at

March 31, 2007, and terminated the interest rate derivatives we had entered into as hedges of the fair value. We replaced

a portion of these securities with an additional $5.4 billion of treasury bills classified as trading and $1.8 billion of

30-year fixed rate MBS classified as available for sale. In addition, we reduced wholesale overnight funding by

approximately $4 billion. The 30-year fixed-rate MBS were a similar asset type to the securities that remained classified

as available for sale but were substantially different from the securities reclassified to trading as part of our adoption.

These securities yielded over 5.5% and had a duration of approximately 5.7%.

Subsequent to the transactions executed at the end of the first quarter and early second quarter, we continued to maintain

an active trading portfolio, as well as refine our trading securities strategies. As trading securities matured or sold, we

purchased additional trading securities that included longer dated agency debentures, commercial paper, ABS, corporate

bonds, etc. During the year ended December 31, 2007, we purchased approximately $23 billion of trading securities for

balance sheet management purposes. In addition, during 2007, we entered into $4.6 billion of FHLB letters of credit that

we elected to record at fair value and used these letters of credit to satisfy customer collateral and deposit requirements.

21