MetLife 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

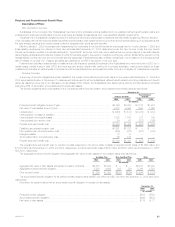

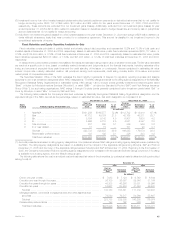

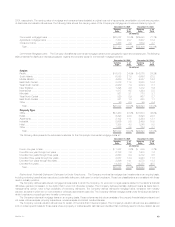

Gross benefit payments and gross subsidy payments under the Prescription Drug Act for the next ten years, which reflect expected future service as

appropriate, are expected to be as follows:

Prescription Net

Postretirement Drug Act Postretirement

Benefits Subsidies Benefits

(In millions)

2006 ************************************************************************* $128 $11 $117

2007 ************************************************************************* $133 $12 $121

2008 ************************************************************************* $138 $13 $125

2009 ************************************************************************* $144 $13 $131

2010 ************************************************************************* $150 $14 $136

2011-2015 ******************************************************************** $833 $83 $750

Insolvency Assessments

Most of the jurisdictions in which the Company is admitted to transact business require life insurers doing business within the jurisdiction to

participate in guaranty associations, which are organized to pay contractual benefits owed pursuant to insurance policies issued by impaired, insolvent or

failed life insurers. These associations levy assessments, up to prescribed limits, on all member insurers in a particular state on the basis of the

proportionate share of the premiums written by member insurers in the lines of business in which the impaired, insolvent or failed insurer engaged. Some

states permit member insurers to recover assessments paid through full or partial premium tax offsets. Assessments levied against the Company were

$4 million, $10 million and $6 million for the years ended December 31, 2005, 2004 and 2003, respectively. The Company maintained a liability of $90

million, and a related asset for premium tax offsets of $54 million, at December 31, 2005 for undiscounted future assessments in respect of currently

impaired, insolvent or failed insurers.

In the past five years, none of the aggregate assessments levied against MetLife’s insurance subsidiaries has been material. The Company has

established liabilities for guaranty fund assessments that it considers adequate for assessments with respect to insurers that are currently subject to

insolvency proceedings.

Effects of Inflation

The Company does not believe that inflation has had a material effect on its consolidated results of operations, except insofar as inflation may affect

interest rates.

Application of Recent Accounting Pronouncements

In February 2006, the FASB issued SFAS No. 155, Accounting for Certain Hybrid Instruments (‘‘SFAS 155’’). SFAS 155 amends SFAS No. 133,

Accounting for Derivative Instruments and Hedging (‘‘SFAS 133’’) and SFAS No. 140, Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities (‘‘SFAS 140’’). SFAS 155 allows financial instruments that have embedded derivatives to be accounted for as a whole,

eliminating the need to bifurcate the derivative from its host, if the holder elects to account for the whole instrument on a fair value basis. In addition,

among other changes, SFAS 155 (i) clarifies which interest-only strips and principal-only strips are not subject to the requirements of SFAS 133;

(ii) establishes a requirement to evaluate interests in securitized financial assets to identify interests that are freestanding derivatives or that are hybrid

financial instruments that contain an embedded derivative requiring bifurcation; (iii) clarifies that concentrations of credit risk in the form of subordination

are not embedded derivatives; and (iv) eliminates the prohibition on a qualifying special-purpose entity (‘‘QSPE’’) from holding a derivative financial

instrument that pertains to a beneficial interest other than another derivative financial interest. SFAS 155 will be applied prospectively and is effective for all

financial instruments acquired or issued for fiscal years beginning after September 15, 2006. SFAS 155 is not expected to have a material impact on the

Company’s consolidated financial statements.

The FASB has issued additional guidance relating to derivative financial instruments as follows:

)In June 2005, the FASB cleared SFAS 133 Implementation Issue No. B38, Embedded Derivatives: Evaluation of Net Settlement with Respect to

the Settlement of a Debt Instrument through Exercise of an Embedded Put Option or Call Option (‘‘Issue B38’’) and SFAS 133 Implementation

Issue No. B39, Embedded Derivatives: Application of Paragraph 13(b) to Call Options That Are Exercisable Only by the Debtor (‘‘Issue B39’’).

Issue B38 clarified that the potential settlement of a debtor’s obligation to a creditor occurring upon exercise of a put or call option meets the net

settlement criteria of SFAS No. 133. Issue B39 clarified that an embedded call option, in which the underlying is an interest rate or interest rate

index, that can accelerate the settlement of a debt host financial instrument should not be bifurcated and fair valued if the right to accelerate the

settlement can be exercised only by the debtor (issuer/borrower) and the investor will recover substantially all of its initial net investment. Issues

B38 and B39, which must be adopted as of the first day of the first fiscal quarter beginning after December 15, 2005, did not have a material

impact on the Company’s consolidated financial statements.

)Effective October 1, 2003, the Company adopted Issue B36. Issue B36 concluded that (i) a company’s funds withheld payable and/or receivable

under certain reinsurance arrangements; and (ii) a debt instrument that incorporates credit risk exposures that are unrelated or only partially related

to the creditworthiness of the obligor include an embedded derivative feature that is not clearly and closely related to the host contract. Therefore,

the embedded derivative feature is measured at fair value on the balance sheet and changes in fair value are reported in income. As a result of the

adoption of Issue B36, the Company recorded a cumulative effect of a change in accounting of $26 million, net of income taxes, for the year

ended December 31, 2003.

)Effective July 1, 2003, the Company adopted SFAS No. 149, Amendment of Statement 133 on Derivative Instruments and Hedging Activities

(‘‘SFAS 149’’). SFAS 149 amended and clarified the accounting and reporting for derivative instruments, including certain derivative instruments

embedded in other contracts, and for hedging activities. Except for certain previously issued and effective guidance, SFAS 149 was effective for

contracts entered into or modified after June 30, 2003. The Company’s adoption of SFAS 149 did not have a significant impact on its

consolidated financial statements.

Effective November 9, 2005, the Company prospectively adopted the guidance in FASB Staff Position (‘‘FSP’’) FAS 140-2, Clarification of the

Application of Paragraphs 40(b) and 40(c) of FAS 140 (‘‘FSP 140-2’’). FSP 140-2 clarified certain criteria relating to derivatives and beneficial interests

when considering whether an entity qualifies as a QSPE. Under FSP 140-2, the criteria must only be met at the date the QSPE issues beneficial interests

or when a derivative financial instrument needs to be replaced upon the occurrence of a specified event outside the control of the transferor. FSP 140-2

did not have a material impact on the Company’s consolidated financial statements.

MetLife, Inc.

40