MetLife 2005 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2005 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

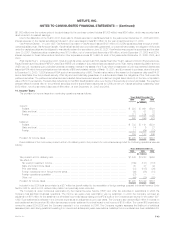

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

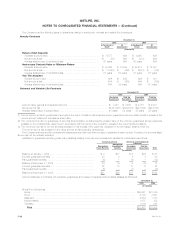

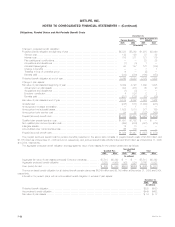

claims in 2004. Accordingly, Metropolitan Life now reports that it received approximately 23,900 asbestos-related claims in 2004. The total number of

asbestos personal injury claims pending against Metropolitan Life as of the dates indicated, the number of new claims during the years ended on those

dates and the total settlement payments made to resolve asbestos personal injury claims during those years are set forth in the following table:

At or For the Years Ended December 31,

2005 2004 2003

(Dollars in millions)

Asbestos personal injury claims at year end (approximate) ************************************ 100,250 108,000 111,700

Number of new claims during the year (approximate) **************************************** 18,500 23,900 58,750

Settlement payments during the year(1) *************************************************** $ 74.3 $ 85.5 $ 84.2

(1) Settlement payments represent payments made by Metropolitan Life during the year in connection with settlements made in that year and in prior

years. Amounts do not include Metropolitan Life’s attorneys’ fees and expenses and do not reflect amounts received from insurance carriers.

The Company believes adequate provision has been made in its consolidated financial statements for all probable and reasonably estimable losses

for asbestos-related claims. The ability of Metropolitan Life to estimate its ultimate asbestos exposure is subject to considerable uncertainty due to

numerous factors. The availability of data is limited and it is difficult to predict with any certainty numerous variables that can affect liability estimates,

including the number of future claims, the cost to resolve claims, the disease mix and severity of disease, the jurisdiction of claims filed, tort reform efforts

and the impact of any possible future adverse verdicts and their amounts.

The number of asbestos cases that may be brought or the aggregate amount of any liability that Metropolitan Life may ultimately incur is uncertain.

Accordingly, it is reasonably possible that the Company’s total exposure to asbestos claims may be greater than the liability recorded by the Company in

its consolidated financial statements and that future charges to income may be necessary. While the potential future charges could be material in

particular quarterly or annual periods in which they are recorded, based on information currently known by management, management does not believe

any such charges are likely to have a material adverse effect on the Company’s consolidated financial position.

Metropolitan Life increased its recorded liability for asbestos-related claims by $402 million from approximately $820 million to $1,225 million at

December 31, 2002. This total recorded asbestos-related liability (after the self-insured retention) was within the coverage of the excess insurance

policies discussed below. Metropolitan Life regularly reevaluates its exposure from asbestos litigation and has updated its liability analysis for asbestos-

related claims through December 31, 2005.

During 1998, Metropolitan Life paid $878 million in premiums for excess insurance policies for asbestos-related claims. The excess insurance

policies for asbestos-related claims provide for recovery of losses up to $1,500 million, which is in excess of a $400 million self-insured retention. The

asbestos-related policies are also subject to annual and per-claim sublimits. Amounts are recoverable under the policies annually with respect to claims

paid during the prior calendar year. Although amounts paid by Metropolitan Life in any given year that may be recoverable in the next calendar year under

the policies will be reflected as a reduction in the Company’s operating cash flows for the year in which they are paid, management believes that the

payments will not have a material adverse effect on the Company’s liquidity.

Each asbestos-related policy contains an experience fund and a reference fund that provides for payments to Metropolitan Life at the commutation

date if the reference fund is greater than zero at commutation or pro rata reductions from time to time in the loss reimbursements to Metropolitan Life if the

cumulative return on the reference fund is less than the return specified in the experience fund. The return in the reference fund is tied to performance of

the Standard & Poor’s 500 Index and the Lehman Brothers Aggregate Bond Index. A claim with respect to the prior year was made under the excess

insurance policies in 2003, 2004 and 2005 for the amounts paid with respect to asbestos litigation in excess of the retention. As the performance of the

indices impacts the return in the reference fund, it is possible that loss reimbursements to the Company and the recoverable with respect to later periods

may be less than the amount of the recorded losses. Such foregone loss reimbursements may be recovered upon commutation depending upon future

performance of the reference fund. If at some point in the future, the Company believes the liability for probable and reasonably estimable losses for

asbestos-related claims should be increased, an expense would be recorded and the insurance recoverable would be adjusted subject to the terms,

conditions and limits of the excess insurance policies. Portions of the change in the insurance recoverable would be recorded as a deferred gain and

amortized into income over the estimated remaining settlement period of the insurance policies. The foregone loss reimbursements were approximately

$8.3 million with respect to 2002 claims, $15.5 million with respect to 2003 claims and $15.1 million with respect to 2004 claims and estimated as of

December 31, 2005, to be approximately $45.4 million in the aggregate, including future years.

Property and Casualty Actions

A purported class action has been filed against Metropolitan Property and Casualty Insurance Company’s (‘‘MPC’’) subsidiary, Metropolitan Casualty

Insurance Company, in Florida alleging breach of contract and unfair trade practices with respect to allowing the use of parts not made by the original

manufacturer to repair damaged automobiles. Discovery is ongoing and a motion for class certification is pending. Two purported nationwide class

actions have been filed against MPC in Illinois. One suit claims breach of contract and fraud due to the alleged underpayment of medical claims arising

from the use of a purportedly biased provider fee pricing system. A motion for class certification has been filed and discovery is ongoing. The second suit

claims breach of contract and fraud arising from the alleged use of preferred provider organizations to reduce medical provider fees covered by the

medical claims portion of the insurance policy. The court recently granted MPC’s motion to dismiss the fraud claim in the second suit.

A purported class action has been filed against MPC in Montana. This suit alleges breach of contract and bad faith for not aggregating medical

payment and uninsured coverages provided in connection with the several vehicles identified in insureds’ motor vehicle policies. A recent decision by the

Montana Supreme Court in a suit involving another insurer determined that aggregation is required. The parties have reached an agreement to settle this

suit. MPC has recorded a liability in an amount the Company believes is adequate to resolve the claims underlying this matter. The amount to be paid will

not be material to MPC. Certain plaintiffs’ lawyers in another action have alleged that the use of certain automated databases to provide total loss vehicle

valuation methods was improper. MPC, along with a number of other insurers, agreed in July 2005 to resolve this issue in a class action format.

Management believes that the amount to be paid in resolution of this matter will not be material to MPC.

In December 2005, a purported class action was filed against MPC in Louisiana federal court on behalf of insureds who incurred total property

losses as a result of Hurricane Katrina. Plaintiffs claim they are entitled to coverage for all of their claims. A lawsuit was filed against MPC in November

2005 in Mississippi federal court by two policyholders challenging the denial of a claim under their homeowners policy for damage caused to their

MetLife, Inc.

F-46