MetLife 2005 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2005 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

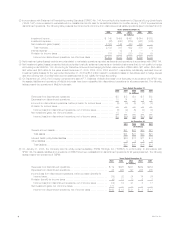

the fair value of the assets acquired and liabilities assumed — the most significant of which relate to the aforementioned critical estimates. In applying

these policies, management makes subjective and complex judgments that frequently require estimates about matters that are inherently uncertain. Many

of these policies, estimates and related judgments are common in the insurance and financial services industries; others are specific to the Company’s

businesses and operations. Actual results could differ from these estimates.

Investments

The Company’s principal investments are in fixed maturities, mortgage and consumer loans, other limited partnerships, and real estate and real

estate joint ventures, all of which are exposed to three primary sources of investment risk: credit, interest rate and market valuation. The financial

statement risks are those associated with the recognition of impairments and income, as well as the determination of fair values. The assessment of

whether impairments have occurred is based on management’s case-by-case evaluation of the underlying reasons for the decline in fair value.

Management considers a wide range of factors about the security issuer and uses its best judgment in evaluating the cause of the decline in the

estimated fair value of the security and in assessing the prospects for near-term recovery. Inherent in management’s evaluation of the security are

assumptions and estimates about the operations of the issuer and its future earnings potential. Considerations used by the Company in the impairment

evaluation process include, but are not limited to: (i) the length of time and the extent to which the market value has been below cost or amortized cost;

(ii) the potential for impairments of securities when the issuer is experiencing significant financial difficulties; (iii) the potential for impairments in an entire

industry sector or sub-sector; (iv) the potential for impairments in certain economically depressed geographic locations; (v) the potential for impairments of

securities where the issuer, series of issuers or industry has suffered a catastrophic type of loss or has exhausted natural resources; (vi) the Company’s

ability and intent to hold the security for a period of time sufficient to allow for the recovery of its value to an amount equal to or greater than cost or

amortized cost; (vii) unfavorable changes in forecasted cash flows on asset-backed securities; and (viii) other subjective factors, including concentrations

and information obtained from regulators and rating agencies. In addition, the earnings on certain investments are dependent upon market conditions,

which could result in prepayments and changes in amounts to be earned due to changing interest rates or equity markets. The determination of fair

values in the absence of quoted market values is based on: (i) valuation methodologies; (ii) securities the Company deems to be comparable; and

(iii) assumptions deemed appropriate given the circumstances. The use of different methodologies and assumptions may have a material effect on the

estimated fair value amounts. In addition, the Company enters into certain structured investment transactions, real estate joint ventures and limited

partnerships for which the Company may be deemed to be the primary beneficiary and, therefore, may be required to consolidate such investments. The

accounting rules for the determination of the primary beneficiary are complex and require evaluation of the contractual rights and obligations associated

with each party involved in the entity, an estimate of the entity’s expected losses and expected residual returns and the allocation of such estimates to

each party.

Derivatives

The Company enters into freestanding derivative transactions primarily to manage the risk associated with variability in cash flows or changes in fair

values related to the Company’s financial assets and liabilities. The Company also uses derivative instruments to hedge its currency exposure associated

with net investments in certain foreign operations. The Company also purchases investment securities, issues certain insurance policies and engages in

certain reinsurance contracts that have embedded derivatives. The associated financial statement risk is the volatility in net income which can result from

(i) changes in fair value of derivatives not qualifying as accounting hedges; (ii) ineffectiveness of designated hedges; and (iii) counterparty default. In

addition, there is a risk that embedded derivatives requiring bifurcation are not identified and reported at fair value in the consolidated financial statements.

Accounting for derivatives is complex, as evidenced by significant authoritative interpretations of the primary accounting standards which continue to

evolve, as well as the significant judgments and estimates involved in determining fair value in the absence of quoted market values. These estimates are

based on valuation methodologies and assumptions deemed appropriate under the circumstances. Such assumptions include estimated volatility and

interest rates used in the determination of fair value where quoted market values are not available. The use of different assumptions may have a material

effect on the estimated fair value amounts.

Deferred Policy Acquisition Costs and Value of Business Acquired

The Company incurs significant costs in connection with acquiring new and renewal insurance business. These costs, which vary with and are

primarily related to the production of that business, are deferred. The recovery of DAC is dependent upon the future profitability of the related business.

The amount of future profit is dependent principally on investment returns in excess of the amounts credited to policyholders, mortality, morbidity,

persistency, interest crediting rates, expenses to administer the business, creditworthiness of reinsurance counterparties and certain economic variables,

such as inflation. Of these factors, the Company anticipates that investment returns are most likely to impact the rate of amortization of such costs. The

aforementioned factors enter into management’s estimates of gross margins and profits, which generally are used to amortize such costs. VOBA,

included in DAC, reflects the estimated fair value of in-force contracts in a life insurance company acquisition and represents the portion of the purchase

price that is allocated to the value of the right to receive future cash flows from the insurance and annuity contracts in force at the acquisition date. VOBA

is based on actuarially determined projections, by each block of business, of future policy and contract charges, premiums, mortality and morbidity,

separate account performance, surrenders, operating expenses, investment returns and other factors. Actual experience on the purchased business

may vary from these projections. Revisions to estimates result in changes to the amounts expensed in the reporting period in which the revisions are

made and could result in the impairment of the asset and a charge to income if estimated future gross margins and profits are less than amounts

deferred. In addition, the Company utilizes the reversion to the mean assumption, a common industry practice, in its determination of the amortization of

DAC. This practice assumes that the expectation for long-term appreciation in equity markets is not changed by minor short-term market fluctuations, but

that it does change when large interim deviations have occurred.

Goodwill

Goodwill is the excess of cost over the fair value of net assets acquired. The Company tests goodwill for impairment at least annually or more

frequently if events or circumstances, such as adverse changes in the business climate, indicate that there may be justification for conducting an interim

test. Impairment testing is performed using the fair value approach, which requires the use of estimates and judgment, at the ‘‘reporting unit’’ level. A

reporting unit is the operating segment, or a business that is one level below the operating segment if discrete financial information is prepared and

regularly reviewed by management at that level. For purposes of goodwill impairment testing, goodwill within Corporate & Other is allocated to reporting

units within the Company’s business segments. If the carrying value of a reporting unit’s goodwill exceeds its fair value, the excess is recognized as an

MetLife, Inc. 7