MetLife 2005 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2005 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

|

|

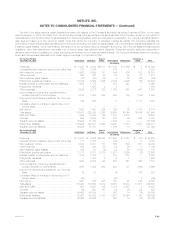

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

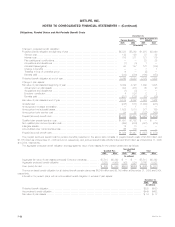

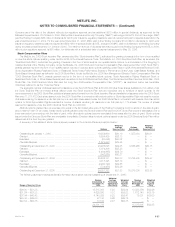

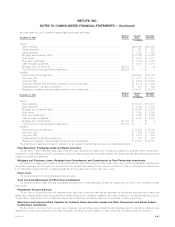

Effective January 1, 2003, the Company elected to prospectively apply the fair value method of accounting for stock options granted by the

Company subsequent to December 31, 2002. As permitted under SFAS 148, stock options granted prior to January 1, 2003 will continue to be

accounted for under APB 25. Had compensation expense for grants awarded prior to January 1, 2003 been determined based on fair value at the date

of grant in accordance with SFAS 123, the Company’s earnings and earnings per common share amounts would have been reduced to the following pro

forma amounts:

Years Ended December 31,

2005 2004 2003

(In millions, except per share

data)

Net income ********************************************************************************* $4,714 $2,758 $2,217

Preferred stock dividend*********************************************************************** 63 — —

Charge for conversion of company-obligated mandatorily redeemable securities of a subsidiary trust(1) ***** ——21

Net income available to common shareholders **************************************************** $4,651 $2,758 $2,196

Add: Stock option-based employee compensation expense included in reported net income, net of income

taxes ************************************************************************************* $33$26$11

Deduct: Total stock option-based employee compensation determined under fair value based method for all

awards, net of income taxes ***************************************************************** $ (35) $ (44) $ (40)

Pro forma net income available to common shareholders(2) ***************************************** $4,649 $2,740 $2,167

Basic earnings per common share

As reported ********************************************************************************* $ 6.21 $ 3.67 $ 2.97

Pro forma(2) ********************************************************************************* $ 6.21 $ 3.65 $ 2.93

Diluted earnings per common share

As reported ********************************************************************************* $ 6.16 $ 3.65 $ 2.94

Pro forma(2) ********************************************************************************* $ 6.15 $ 3.63 $ 2.90

(1) See Note 10 for a discussion of this charge included in the calculation of net income available to common shareholders.

(2) The pro forma earnings disclosures are not necessarily representative of the effects on net income and earnings per share in future years.

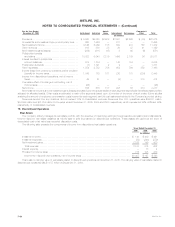

Prior to January 1, 2005, the Black-Scholes model was used to determine the fair value of options granted as recognized in the financial statements

or as reported in the pro forma disclosure above. The fair value of stock options issued on or after January 1, 2005 was estimated on the date of grant

using a binomial lattice model. The Company made this change because lattice models produce more accurate option values due to the ability to

incorporate assumptions about employee exercise behavior resulting from changes in the price of the underlying shares. In addition, lattice models allow

for changes in critical assumptions over the life of the option in comparison to closed-form models like Black-Scholes, which require single-value

assumptions at the time of grant.

The expected volatility used in the binomial lattice model is based on an analysis of historical prices of the Company’s common stock and options on

the Company’s shares traded on the open market. The Company used a weighted-average of the implied volatility for traded call options with the longest

remaining maturity nearest to the money as of each valuation date and the historical volatility, calculated using monthly share prices. The Company chose

a monthly measurement interval for historical volatility as it believes this better depicts the nature of employee option exercise decisions being based on

longer-term trends in the price of the Company’s shares rather than on daily price movements.

The risk-free rate is based on observed interest rates for instruments with maturities similar to the expected term of the employee stock options. The

Black-Scholes model requires a single spot rate, therefore the weighted-average of these rates for all grants in the year indicated is presented in the table

below. The binomial lattice model allows for the use of different rates for different years. The table below presents the range of imputed forward rates for

U.S. Treasury Strips that was input over the contractual term of the options.

Dividend yield is determined based on historical dividend distributions compared to the price of the underlying shares as of the valuation date,

adjusted for any expected future changes in the dividend rate. For options valued using the binomial lattice model during the year ended December 31,

2005, the dividend yield as of the measurement date was held constant throughout the life of the option.

Use of the Black-Scholes model requires an input of the expected life of the options, or the average number of years before options will be exercised

or expired. The Company estimated expected life using the historical average years to exercise or cancellation and average remaining years outstanding

for vested options. Alternatively, the binomial model used by the Company incorporates the contractual term of the options and then considers expected

exercise behavior and a post-vesting termination rate, or the rate at which vested options are exercised or expire prematurely due to termination of

employment, to derive an expected life. Exercise behavior in the Company’s binomial lattice model is expressed using an exercise multiple, which reflects

the ratio of exercise price to the strike price of options granted at which employees are expected to exercise. The exercise multiple is derived from actual

historical exercise activity.

MetLife, Inc.

F-58