MetLife 2005 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2005 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

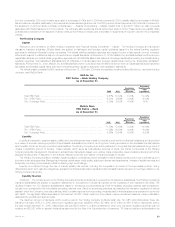

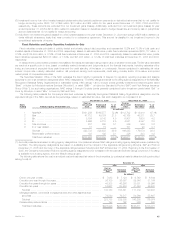

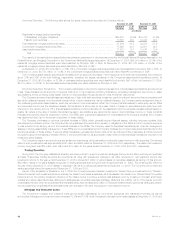

The weighted average and weighted average target allocation of pension plan assets within the separate accounts is as follows:

December 31,

Weighted

Weighted Average Target

Average Allocation

2005 2004 2006

Asset Category

Equity securities **************************************************************************** 47% 50% 30%-65%

Fixed maturities ***************************************************************************** 37% 36% 20%-70%

Other (Real Estate and Alternative Investments)*************************************************** 16% 14% 0%-25%

Total ************************************************************************************ 100% 100%

Target allocations of assets are determined with the objective of maximizing returns and minimizing volatility of net assets through adequate asset

diversification. Adjustments are made to target allocations based on an assessment of the impact of economic factors and market conditions.

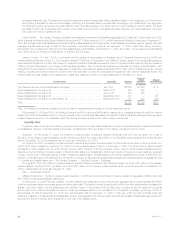

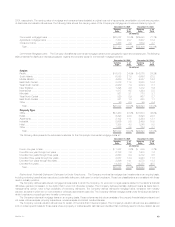

Postretirement Benefit Plan Assets

Assets of the postretirement benefit plans are invested within life insurance and reserve contracts issued by the Subsidiaries. The majority of assets

are held in separate accounts established by the Subsidiaries. The account values of assets held with the Subsidiaries were $1,039 million and

$1,011 million as of December 31, 2005 and 2004, respectively. The terms of these contracts are consistent in all material respects with what the

Subsidiaries offer to unaffiliated parties who are similarly situated.

The valuation of separate accounts and the investments within such separate accounts invested in by the postretirement plans are similar to that

described in the preceding section on pension plans.

The weighted average and weighted average target allocation of other postretirement benefit plan assets within the separate account is as follows:

December 31,

Weighted

Weighted Average

Average Target Allocation

2005 2004 2006

Asset Category

Equity securities ************************************************************************* 42% 41% 30%-45%

Fixed maturities************************************************************************** 53% 57% 45%-70%

Other ********************************************************************************** 5% 2% 0%-10%

Total ********************************************************************************* 100% 100%

Target allocations of assets are determined with the objective of maximizing returns and minimizing volatility of net assets through adequate asset

diversification. Adjustments are made to target allocations based on an assessment of the impact of economic factors and market conditions.

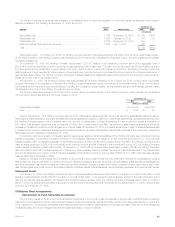

Funding and Cash Flows of Pension and Postretirement Benefit Plan Obligations

Pension Plan Obligations

It is the Subsidiaries’ practice to make contributions to the qualified pension plan to comply with minimum funding requirements of Employee

Retirement Income Security Act of 1974, as amended, and/or to maintain a fully funded accumulated benefit obligation. In accordance with such

practice, no contributions were required for the year ended December 31, 2005 and no contributions are anticipated to be required for 2006. The non-

qualified pension plans are funded as benefit payments become due under the provision of the plans. The Subsidiaries expect to make discretionary

contributions of $187 million towards the pension plans in 2006. Gross pension benefit payments for the next ten years, which reflect expected future

service as appropriate, are expected to be as follows:

Pension

Benefits

(In millions)

2006 ******************************************************************************************************* $320

2007 ******************************************************************************************************* $325

2008 ******************************************************************************************************* $337

2009 ******************************************************************************************************* $351

2010 ******************************************************************************************************* $355

2011-2015************************************************************************************************** $1,984

Postretirement Benefit Plan Obligations

Postretirement benefits represent a non-vested, non-guaranteed obligation of the Subsidiaries and current regulations do not require specific funding

levels for these benefits. While the Subsidiaries have funded such plans in advance, it has been the Subsidiaries’ practice to use their general assets to

pay claims as they come due instead of utilizing plan assets.

The Subsidiaries expect to make discretionary contributions of $128 million, based upon expected gross benefit payments, towards the postretire-

ment plan obligations in 2006. As noted previously, the Subsidiaries expect to receive subsidies under the Prescription Drug Act to offset such

payments.

MetLife, Inc. 39