ICICI Bank 2013 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

66

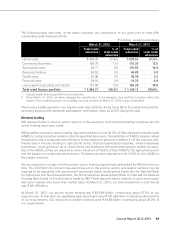

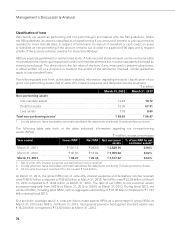

The following table sets forth, at the dates indicated, the capital adequacy ratios computed in accordance

with the RBI guidelines on Basel II.

` in billion, except percentages

At March 31, 2012 At March 31, 2013

Tier-1 capital ` 505.18 ` 565.62

Tier-2 capital 232.95 262.74

Total capital 738.13 828.36

Credit Risk — Risk Weighted Assets (RWA) 3,468.74 3,894.82

Market Risk — RWA 268.66 254.68

Operational Risk — RWA 248.46 269.94

Total RWA ` 3,985.86 ` 4,419.44

Total capital adequacy ratio 18.52% 18.74%

Tier-1 capital adequacy ratio 12.68% 12.80%

Tier-2 capital adequacy ratio 5.84% 5.94%

Movement in our capital funds and risk weighted assets from March 31, 2012 to March 31, 2013

During fiscal 2013, capital funds (net of deductions) increased by ` 90.23 billion from ` 738.13 billion

at March 31, 2012 to ` 828.36 billion at March 31, 2013. The increase in the capital funds was due

to accretion to retained earnings, issuance of lower Tier-2 capital instruments, lower deduction from

capital funds on account of securitisation exposures and repatriation of capital from an overseas banking

subsidiary.

Credit risk RWA increased by ` 426.08 billion from ` 3,468.74 billion at March 31, 2012 to ` 3,894.82 billion

at March 31, 2013 primarily due to increase of ` 369.53 billion in RWA for on-balance sheet exposures,

offset, in part, by decrease of ` 56.55 billion in RWA for off-balance sheet credit exposures.

Market risk RWA decreased by ` 13.98 billion from ` 268.66 billion at March 31, 2012 to ` 254.68 billion

at March 31, 2013. The general market risk RWA decreased by ` 11.44 billion (capital charge of ` 1.03

billion).

The operational risk RWA at March 31, 2013 was ` 269.94 billion (capital charge of ` 24.29 billion). The

operational risk capital charge is computed based on 15% of average of previous three financial years’

gross income and is revised on an annual basis at June 30.

Internal assessment of capital

Our capital management framework includes a comprehensive internal capital adequacy assessment

process conducted annually, which determines the adequate level of capitalisation necessary to meet

regulatory norms and current and future business needs, including under stress scenarios. The internal

capital adequacy assessment process is formulated at both standalone bank level and the consolidated

group level. The internal capital adequacy assessment process encompasses capital planning for a four

year time horizon, identification and measurement of material risks and the relationship between risk

and capital.

The capital management framework is complemented by the risk management framework, which includes

a comprehensive assessment of material risks. Stress testing, which is a key aspect of the internal capital

adequacy assessment process and the risk management framework, provides an insight on the impact

Management’s Discussion & Analysis