ICICI Bank 2013 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

F27

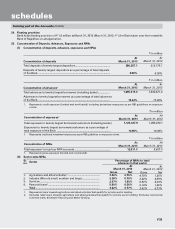

The Bank has exposure in credit derivative instruments including credit default swaps (CDS), credit linked notes,

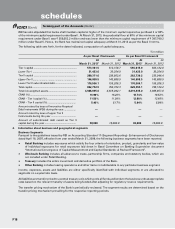

collateralised debt obligations and principal protected structures. The notional principal amount of these credit derivatives

outstanding at March 31, 2013 was Nil (March 31, 2012: Nil) in funded instrument and ` 3,065.6 million (March 31, 2012:

` 10,349.9 million) in non-funded instruments. The profit and loss impact on the above portfolio on account of mark-to-

market and realised gain/losses during the year ended March 31, 2013 was net profit of ` 75.0 million (March 31, 2012:

net profit ` 561.0 million). At March 31, 2013, the total outstanding mark-to-market position of the above portfolio was

a net gain of ` 10.8 million (March 31, 2012: net loss of ` 59.6 million). Non Rupee denominated credit derivatives are

marked to market by the Bank based on counter-party valuation quotes, or internal models using inputs from market

sources such as Bloomberg/Reuters, counter-parties and FIMMDA. Rupee denominated credit derivatives are marked to

market by the Bank based on FIMMDA guidelines.

The Bank offers deposits to customers of its offshore branches with structured returns linked to interest, forex, credit or

equity benchmarks. The Bank covers these exposures in the inter-bank market. At March 31, 2013, the net open position

on this portfolio was Nil (March 31, 2012: Nil) with mark-to-market position of ` 13.9 million (March 31, 2012: ` 24.8

million). The profit and loss impact on account of mark-to-market and realised profit and loss during the year ended

March 31, 2013 was a net loss of ` 18.7 million (March 31, 2012: net loss of ` 5.2 million).

The notional principal amount of forex contracts classified as non-trading at March 31, 2013 amounted to ` 526,615.8

million (March 31, 2012: ` 745,722.2 million). For these non-trading forex contracts, at March 31, 2013, marked to market

position was asset of ` 2,855.4 million (March 31, 2012: ` 22,528.9 million) and liability of ` 6,652.4 million (March 31,

2012: ` 12,843.6 million), credit exposure of ` 16,131.9 million (March 31, 2012: ` 42,639.4 million) and likely impact of

one percentage change in interest rate (100*PV01) was ` 52.3 million (March 31, 2012: ` 81.6 million).

The notional principal amount of forex contracts classified as trading at March 31, 2013 amounted to ` 2,311,888.1

million (March 31, 2012: ` 2,814,328.7 million). For these trading forex contracts, at March 31, 2013, marked to market

position was asset of ` 38,526.6 million (March 31, 2012: ` 70,164.7 million) and liability of ` 32,462.9 million (March 31,

2012: ` 66,449.6 million), credit exposure of ` 97,274.0 million (March 31, 2012: ` 135,371.9 million) and likely impact of

one percentage change in interest rate (100*PV01) was ` 58.9 million (March 31, 2012: ` 90.1 million). The net overnight

open position at March 31, 2013 was ` 573.8 million (March 31, 2012: ` 299.1 million).

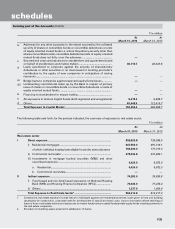

15. Exchange traded interest rate derivatives and currency options

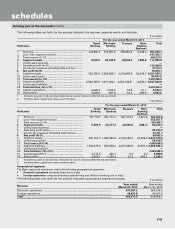

Exchange traded interest rate derivatives

The Bank had no outstanding exchange traded interest rate derivatives March 31, 2013 (March 31, 2012: Nil).

Exchange traded currency options

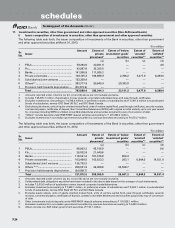

The following table sets forth, for the periods indicated, the details of exchange traded currency options.

` in million

Particulars At

March 31, 2013

At

March 31, 2012

i) Notional principal amount of exchange traded currency options

undertaken during the year ........................................................................... 257,249.4 434,623.3

ii) Notional principal amount of exchange traded currency options

outstanding .................................................................................................... 2,084.3 12,587.8

iii) Notional principal amount of exchange traded currency options

outstanding and not “highly effective” ......................................................... N.A. N.A.

iv) Mark-to-market value of exchange traded currency options outstanding

and not “highly effective” ............................................................................. N.A. N.A.

16. Forward rate agreement (FRA)/Interest rate swaps (IRS)

The Bank enters into FRA and IRS contracts for balance sheet management and market making purposes whereby the

Bank offers derivative products to its customers to enable them to hedge their interest rate risk within the prevalent

regulatory guidelines.

A FRA is a financial contract between two parties to exchange interest payments for a ’notional principal’ amount

on settlement date, for a specified period from start date to maturity date. Accordingly, on the settlement date, cash

payments based on contract rate and the settlement rate, which is the agreed bench-mark/reference rate prevailing on

the settlement date, are made by the parties to one another. The benchmark used in the FRA contracts of the Bank is

London Inter-Bank Offered Rate (LIBOR) of various currencies.

forming part of the Accounts (Contd.)

schedules