ICICI Bank 2013 Annual Report Download - page 183

Download and view the complete annual report

Please find page 183 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

F105

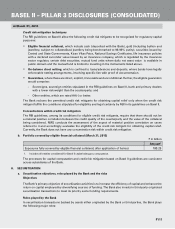

c. credits in the account are not enough to cover the interest debited during the accounting period; or

d. drawings have been permitted in the account for a continuous period of 90 days based on drawing power

computed on the basis of stock statements that are more than three months old even though the unit may

be working or the borrower’s financial position is satisfactory; or

e. the regular/ad hoc credit limits have not been reviewed/renewed within 180 days from the due date/date

of ad hoc sanction.

iv) a bill purchased/discounted by the Bank remains overdue for a period of more than 90 days;

v) interest and/or installment of principal in respect of an agricultural loan remains overdue for two crop seasons

for short duration crops and one crop season for long duration crops;

vi) In respect of a securitisation transaction undertaken in terms of the RBI guidelines on securitisation, the

amount of liquidity facility remains outstanding for more than 90 days;

vii) In respect of derivative transactions, if the overdue receivables representing positive mark-to-market value of

a derivative contract, remain unpaid for a period of 90 days from the specified due date for payment.

Irrespective of payment performance, the Bank identifies a borrower account as a NPA even if it does not meet

any of the above mentioned criteria, where:

• loans availed by a borrower are repeatedly restructured unless otherwise permitted by regulations;

• loans availed by a borrower are classified as fraud;

• project does not commence commercial operations within the timelines permitted under the RBI guidelines

in respect of the loans extended to a borrower for the purpose of implementing a project; and

• any security in nature of debenture/bonds/equity shares issued by a borrower and held by the Bank is

classified as non-performing investment.

Further, NPAs are classified into sub-standard, doubtful and loss assets based on the criteria stipulated by RBI. A

sub-standard asset is one, which has remained a NPA for a period less than or equal to 12 months. An asset is

classified as doubtful if it has remained in the sub-standard category for more than 12 months. A loss asset is one

where loss has been identified by the Bank or internal or external auditors or during RBI inspection but the amount

has not been written off fully.

Restructured assets

As per RBI guidelines, a fully secured standard loan can be restructured by rescheduling principal repayments

and/or the interest element, but must be separately disclosed as a restructured loan in the year of restructuring.

Similar guidelines apply to restructuring of sub-standard and doubtful loans.

A restructured loan will be upgraded to the standard category only after the borrower demonstrates satisfactory

payment performance over a period of time and after the loan reverts to the normal level of standard asset

provisions and risk weights. RBI has specified the period to be one year from the date when the instalment/

interest falls due as per the restructuring scheme.

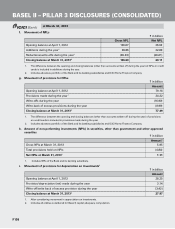

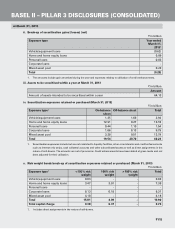

a. Credit risk exposures (March 31, 2013)

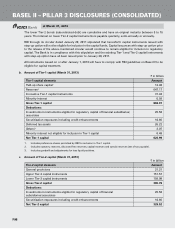

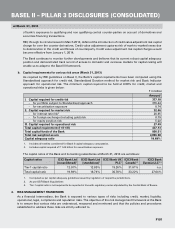

Credit risk exposures (excluding specific risk on available-for-sale and held-for-trading portfolio) include all

credit exposures as per RBI guidelines on exposure norms and investments in the held-to-maturity category.

Exposures to regulatory capital instruments of subsidiaries that are deducted from the capital funds have

been excluded.

` in billion

Category Credit exposure

Fund-based facilities15,871.08

Non-fund based facilities 2,799.49

Total2 8,670.57

1. Includes investment in government securities held under held-to-maturity category.

2. Includes all entities considered for Basel II capital adequacy computation.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2013