ICICI Bank 2013 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

F114

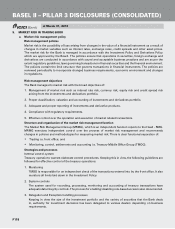

premium arising from securitisation is amortised over the life of the securities issued or to be issued by the

special purpose vehicle to which the assets are sold.

In accordance with the RBI guidelines dated May 7, 2012 for securitisation of standard assets, with effect from

May 7, 2012, the Bank accounts for any loss arising from securitisation immediately at the time of sale and the

profit/premium arising from securitisation is amortised over the life of the transaction based on the method

prescribed in RBI guidelines.

Methods and key assumptions (including inputs) applied in valuing positions retained or purchased

The valuation of the retained interests in the form of pass-through certificates (PTCs) is based on the projected

cash flows as received from the issuer, which are present valued using the Yield-to-Maturity (YTM) rates,

which are computed with a mark-up (reflecting associated credit risk) over the YTM rates for government

securities as published by Fixed Income Money Market and Derivatives Association (FIMMDA).

The retained/purchased interests in the form of subordinate contributions are carried at book value.

There is no change in the methods and key assumptions applied in valuing retained/purchased interests from

previous year.

Policies for recognising liabilities on the balance sheet for arrangements that could require the bank to

provide financial support for securitised assets

The Bank provides credit enhancements in the form of cash deposits or guarantees in its securitisation

transactions. The Bank makes appropriate provisions for any delinquency losses assessed at the time of sale

as well as over the life of the securitisation transactions in accordance with the RBI guidelines.

c. Rating of securitisation exposures

Ratings obtained from ECAIs stipulated by RBI (as stated above) are used for computing capital requirements

for securisation exposures. Where the external ratings of the Bank’s investment in securitised debt

instruments/PTCs are at least partly based on unfunded support provided by the Bank, such investments are

treated as unrated and deducted from the capital funds.

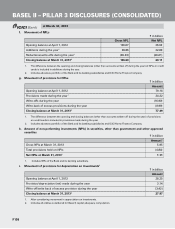

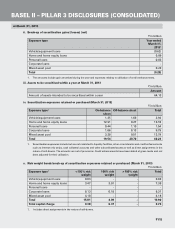

d. Details of securitisation exposures in the banking book

i. Total outstanding exposures securitised by the Bank and the related unrecognised gains/(losses)

(March 31, 2013)

` in billion

Exposure type Outstanding1Unrecognised

gains/(losses)

Vehicle/equipment loans - -

Home and home equity loans 6.71 -

Personal loans - -

Corporate loans 1.82 -

Mixed asset pool - -

Total 8.53 -

1. The amounts represent the total outstanding principal at March 31, 2013 for securitisation deals and include direct

assignments in the nature of sell-downs. Credit enhancements and liquidity facilities are not included in the above

amounts. During the year ended March 31, 2013, the Bank had not securitised any assets as an originator.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2013