ICICI Bank 2013 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

F111

Credit risk mitigation techniques

The RBI guidelines on Basel II allow the following credit risk mitigants to be recognised for regulatory capital

purposes:

• Eligible financial collateral, which include cash (deposited with the Bank), gold (including bullion and

jewellery, subject to collateralised jewellery being benchmarked to 99.99% purity), securities issued by

Central and State Governments, Kisan Vikas Patra, National Savings Certificates, life insurance policies

with a declared surrender value issued by an insurance company, which is regulated by the insurance

sector regulator, certain debt securities, mutual fund units where daily net asset value is available in

public domain and the mutual fund is limited to investing in the instruments listed above.

• On-balance sheet netting, which is confined to loans/advances and deposits, where banks have legally

enforceable netting arrangements, involving specific lien with proof of documentation.

• Guarantees, where these are direct, explicit, irrevocable and unconditional. Further, the eligible guarantors

would comprise:

- Sovereigns, sovereign entities stipulated in the RBI guidelines on Basel II, bank and primary dealers

with a lower risk weight than the counterparty; and

- Other entities, which are rated AA(-) or better.

The Bank reckons the permitted credit risk mitigants for obtaining capital relief only when the credit risk

mitigant fulfills the conditions stipulated for eligibility and legal certainty by RBI in its guidelines on Basel II.

Concentrations within credit risk mitigation

The RBI guidelines, among its conditions for eligible credit risk mitigants, require that there should not be

a material positive correlation between the credit quality of the counterparty and the value of the collateral

being considered. RMG conducts the assessment of the aspect of material positive correlation on cases

referred to it and accordingly evaluates the eligibility of the credit risk mitigant for obtaining capital relief.

Currently, the Bank does not have any concentration risk within credit risk mitigation.

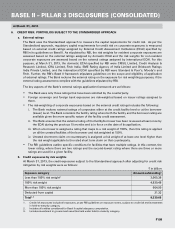

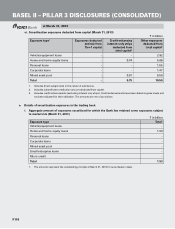

b. Portfolio covered by eligible financial collateral (March 31, 2013)

` in billion

Amount1

Exposures fully covered by eligible financial collateral, after application of haircut 180.25

1. Includes all entities considered for Basel II capital adequacy computation.

The processes for capital computation and credit risk mitigation based on Basel II guidelines are consistent

across subsidiaries of the Bank.

8. SECURITISATION

a. Securitisation objectives, roles played by the Bank and the risks

Objectives

The Bank’s primary objective of securitisation activities is to increase the efficiency of capital and enhance the

return on capital employed by diversifying sources of funding. The Bank also invests in third party originated

securitisation transactions to meet its priority sector lending requirements.

Roles played by the Bank

In securitisation transactions backed by assets either originated by the Bank or third parties, the Bank plays

the following major roles:

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2013