ICICI Bank 2013 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2013 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

F104

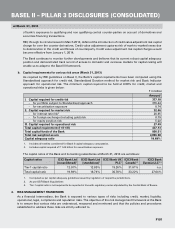

In respect of retail loans, all exposures are approved under operating notes or programs approved by the COED.

This involves a cluster-based approach for a particular product or for homogeneous group of individuals/business

entities that comply with certain laid down parameterised norms. The norms vary across product segments/

customer profile, but typically include factors such as the borrower’s income, the loan-to-value ratio and

demographic parameters. The individual credit proposals are evaluated and approved by executives on the basis

of the product policies.

Credit risk monitoring process

For effective monitoring of credit facilities, a post-approval authorisation structure has been laid down. For

corporate, small enterprises and rural and agriculture linked banking business, Credit Middle Office Group verifies

adherence to the terms of the approval prior to commitment and disbursement of credit facilities.

The Bank has established centralised operations to manage operational risk in the various back office processes

of the Bank’s retail loan business except for a few operations, which are decentralised to improve turnaround

time for customers. The fraud prevention and control group manages fraud-related risks through fraud prevention

and through recovery of fraud losses. The fraud control group evaluates various external agencies involved in

the retail finance operations, including direct marketing associates, external verification associates and collection

agencies.

The Bank has a collections unit structured along various product lines and geographical locations, to manage

delinquency levels. The collections unit operates under the guidelines of a standardised recovery process.

The segregation of responsibilities and oversight by groups external to the business groups ensure adequate

checks and balances.

Reporting and measurement

Credit exposure for the Bank is measured and monitored using a centralised exposure management system. The

analysis of the composition of the portfolio is presented to the Risk Committee on a periodic basis.

The Bank complies with the norms on exposure stipulated by RBI for both single borrower as well as borrower

group at the consolidated level. Limits have been set as a percentage of the Bank’s consolidated capital funds and

are regularly monitored. The utilisation against specified limits is reported to the COED and Credit Committee on

a periodic basis.

Credit concentration risk

Credit concentration risk arises mainly on account of concentration of exposures under various categories

including industry, products, geography, sensitive sectors, underlying collateral nature and single/group borrower

exposures.

Limits have been stipulated on single borrower, borrower group, industry and longer tenure exposure to a

borrower group. Exposure to top 10 borrowers and borrower groups, exposure to capital market segment and

unsecured exposures for the ICICI Group (consolidated) are reported to the senior management committees on a

quarterly basis. Limits on countries and bank counterparties have also been stipulated.

Definition and classification of non-performing assets (NPAs)

The Bank classifies its advances (loans and credit substitutes in the nature of an advance) into performing and

non-performing loans in accordance with the extant RBI guidelines.

An NPA is defined as a loan or an advance where:

i) interest and/or installment of principal remain overdue for more than 90 days in respect of a term loan. Any

amount due to the bank under any credit facility is ‘overdue’ if it is not paid on the due date fixed by the Bank;

ii) if the interest due and charged during a quarter is not serviced fully within 90 days from the end of the quarter;

iii) the account remains ‘out of order’ in respect of an overdraft/cash credit facility. An account is treated as ‘out

of order’ if:

a. the outstanding balance remains continuously in excess of the sanctioned limit/drawing power for 90

days; or

b. where the outstanding balance in the principal operating account is less than the sanctioned limit/drawing

power, but there are no credits continuously for 90 days as on the date of the balance sheet; or

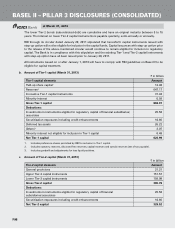

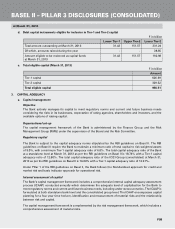

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2013