Volvo 2015 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2015 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

BRL

6.0

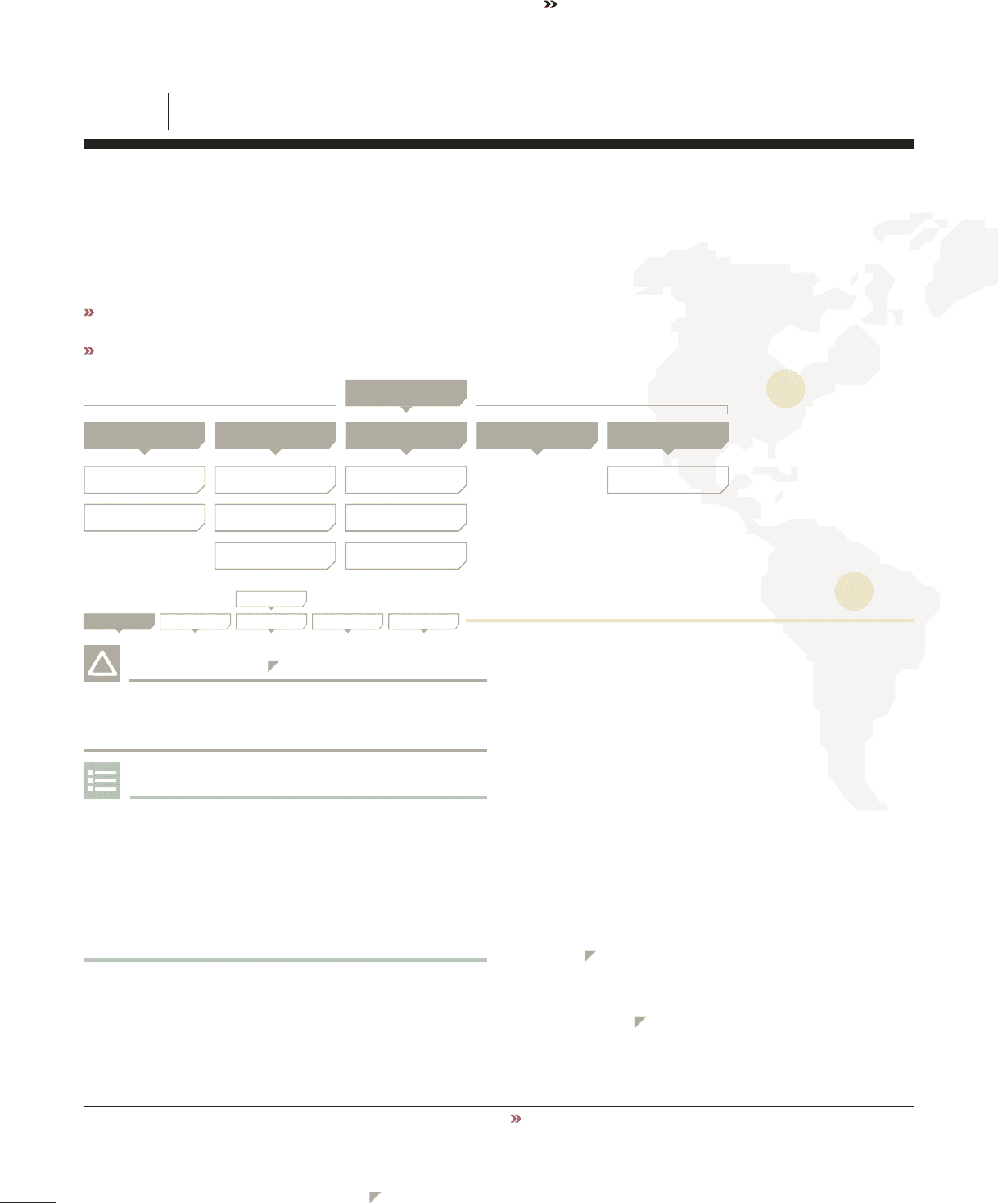

The Volvo Group’s global operations expose the Group to financial risks in

the form of interest rate risks, currency risks, credit risks, liquidity risks

and other price risks. Work on financial risks comprises an integrated

element of the Volvo Group’s business. The Volvo Group strive to minimize

these risks by optimizing the Group’s capital costs by utilizing economies

of scale, minimize negative effects on income as a result of changes in

currency or interest rates and to minimize risk exposure. All risks are man-

aged pursuant to the Volvo Group’s established policies in these areas.

Read more about accounting principles for financial instruments in Note 30,

Financial Instruments.

Read more about management of capital on page 101 and page 102.

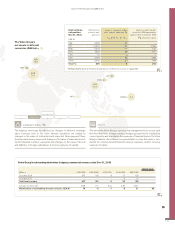

INTEREST-RATE RISKS A

Interest-rate risk refers to the risk that changed interest-rate will affect

the Volvo Group’s consolidated earnings and cash flow (cash-flow risks) or

the fair value of financial assets and liabilities (price risks).

POLICY

Matching the interest-fixing terms of financial assets and liabilities

reduces the exposure. Interest-rate swaps are used to change/influence

the interest-fixing term for the Volvo Group’s financial assets and liabili-

ties. Currency interest-rate swaps enable borrowing in foreign currencies

from different markets without introducing currency risk. The Volvo Group

has also standardized interest-rate forward contracts (futures) and FRAs

(forward-rate agreements). Most of these contracts are used to hedge

interest-rate levels for short-term borrowing or investments.

Cash-flow risks

The effect of changed interest rate levels on future currency and interest-

rate flows primarily pertains to the Volvo Group’s Customer Finance Oper-

ations and net financial items. Customer Finance Operations measure the

degree of matching interest rate fixing on borrowing and lending. The

calculation of the matching degree excludes equity, which amounted to

between 8 and 9% in the Customer Finance Operations. At year-end

2015, the degree of such matching was 99% (101) for the segment

Customer Finance, which was in line with the Volvo Group’s policy. The

centralized Treasury function has, for practical as well as business rea-

sons, the mandate to mismatch the Customer Finance portfolio down to a

matching ratio of 80%. At year-end 2015, the matching ratio was 91%

(110). Any gains or losses from the mismatch impact the segment Group

functions and other within Industrial Operations. At year-end 2015, in

addition to the assets in its Customer Finance Operations, the Volvo

Group’s interest-bearing assets consisted primarily of cash, cash equiva-

lents and liquid assets invested in short-term interest-bearing securities.

The objective for the Volvo Group’s short-term interest-bearing securities

is to achieve a return on these assets equivalent to a three-month fixed

term security. On December 31, 2015, the average interest on Industrial

Operations financial assets was 0.6% (0.9). After taking derivatives into

account, outstanding loans had interest terms corresponding to a short

term interest-rate fixing term, between one to three months. The average

interest on Industrial Operations financial liabilities at year-end amounted

to 4.3% (3.8), including the Volvo Group’s credit costs.

Price risks C

Exposure to price risks as a result of changed interest-rate refers to finan-

cial assets and liabilities with a longer interest-rate fixing term (fixed inter-

est).

The following table 4:1 shows the effect on earnings before taxes in

Industrial Operations net financial position, excluding pensions and similar

obligations, if interest rates were to increase by 1 percentage point, (100

basis points) assuming an average interest-rate fixed term of three months.*

The impact on equity is earnings after tax.

* The sensitivity analysis on interest rate risks is based on simplified assumptions. It is

not improbable for market interest rates to change by one percentage point (100

basis points) on an annual basis. However, in reality, these rates often rise or decline

at different points in time. The sensitivity analysis also assumes a parallel deferment of

the return curve, and that the interest rates on assets and liabilities will be equally

impacted by changes in market interest rates. Accordingly, the impact of real interest -

rate changes may differ from the analysis presented in table 4:1.

Read more in Note 20 Provisions for post-employment benefits regarding

sensitivity analysis on the defined benefit obligations when changes in the applied

assumptions for discount rate and inflations are made.

INTEREST-RATE RISKS CURRENCY RISKS CREDIT RISKS

FINANCIAL RISKS

OTHER PRICE RISKSLIQUIDITY RISKS

NOTE 4 GOALS AND POLICIES IN FINANCIAL RISK MANAGEMENT

CASH-FLOW RISKS

PRICE RISKS FINANCIAL CURRENCY

EXPOSURE

CURRENCY EXPOSURE

OF EQUITY

COMMERCIAL CURRENCY

EXPOSURE COMMERCIAL CREDIT RISK COMMODITY RISK

FINANCIAL CREDIT RISK

FINANCIAL

COUNTERPARTY RISK

INTEREST-RATE RISKS CURRENCY RISKS CREDIT RISKS

FINANCIAL RISKS

OTHER PRICE RISKSLIQUIDITY RISKS

USD

8.7

GROUP PERFORMANCE 2015 NOTES

116