ICICI Bank 2011 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2011 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

F19

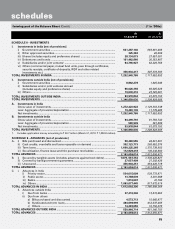

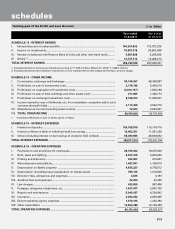

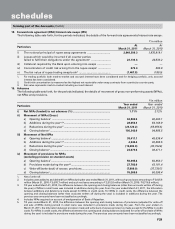

The following table sets forth, for the dates indicated, computation of capital adequacy.

` in million

As per Basel I framework As per Basel II framework

At

March 31, 2011

At

March 31, 2010

At

March 31, 2011

At

March 31, 2010

Tier-1 capital .......................................................... 463,987.9 432,614.3 449,749.1 410,615.1

(Of which Lower Tier-1) ......................................... 28,116.1 28,210.0 28,116.1 28,210.0

Tier-2 capital .......................................................... 231,007.0 181,569.1 217,501.5 160,409.9

(Of which Upper Tier-2) ......................................... 138,248.5 137,912.0 138,248.5 137,912.0

Total capital ............................................................ 694,994.9 614,183.4 667,250.6 571,025.0

Total risk weighted assets ..................................... 3,942,191.1 3,208,425.4 3,414,979.5 2,941,805.8

CRAR (%) ............................................................... 17.63% 19.14% 19.54% 19.41%

CRAR – Tier-1 capital (%) ...................................... 11.77% 13.48% 13.17% 13.96%

CRAR – Tier-2 capital (%) ...................................... 5.86% 5.66% 6.37% 5.45%

During the year ended March 31, 2011, the Bank raised subordinated debt qualifying for Tier-2 capital amounting to

` 59,790.0 million (March 31, 2010: ` 62,000.0 million). This included an issuance of ` 25,000.0 million, wherein the funds

were received in March 2010 but were not considered for Tier-2 capital pending allotment.

5. Information about business and geographical segments

Business Segments

Pursuant to the guidelines issued by RBI on Accounting Standard 17 – (Segment Reporting) - Enhancement of Disclosures

dated April 18, 2007, effective from year ended March 31, 2008, the following business segments have been reported.

•Retail Banking includes exposures which satisfy the four criteria of orientation, product, granularity and low value

of individual exposures for retail exposures laid down in Basel Committee on Banking Supervision document

“International Convergence of Capital Measurement and Capital Standards: A Revised Framework”.

•Wholesale Banking includes all advances to trusts, partnership firms, companies and statutory bodies, which are

not included under Retail Banking.

•Treasury includes the entire investment portfolio of the Bank.

•Other Banking includes hire purchase and leasing operations and other items not attributable to any particular

business segment.

Income, expenses, assets and liabilities are either specifically identified with individual segments or are allocated to

segments on a systematic basis.

All liabilities are transfer priced to a central treasury unit, which pools all funds and lends to the business units at appropriate

rates based on the relevant maturity of assets being funded after adjusting for regulatory reserve requirements.

forming part of the Accounts (Contd.)

schedules