ICICI Bank 2011 Annual Report Download - page 187

Download and view the complete annual report

Please find page 187 of the 2011 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

F109

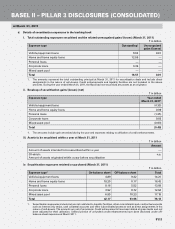

• Investor/trader/market-maker: acquiring investment grade securitised debt instruments backed by financial

assets originated by third parties for purposes of investment/trading/market-making with the aim of developing

an active secondary market in securitised debt.

• Structurer: structuring appropriately in a form and manner suitably tailored to meet investor requirements

while being compliant with extant regulations.

• Provider of liquidity facilities: addressing temporary mismatches on account of the timing differences

between the receipt of cash flows from the underlying performing assets and the fulfillment of obligations to

the beneficiaries.

• Provider of credit enhancement facilities: addressing delinquencies associated with the underlying assets,

i.e. bridging the gaps arising out of credit considerations between cash flows received/collected from the

underlying assets and the fulfillment of repayment obligations to the beneficiaries.

• Provider of collection and processing services: collecting and/or managing receivables from underlying

obligors, contribution from the investors to securitisation transactions, making payments to counterparties/

appropriate beneficiaries, reporting the collection efficiency and other performance parameters and providing

other services relating to collections and payments as may be required for the purpose of the transactions.

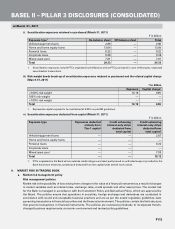

Risks in securitisation

The major risks inherent in the securitised transactions are:

• Credit risk: Risk arising on account of payment delinquencies from underlying obligors/borrowers in the

assigned pool.

• Market risk:

i) Liquidity risk: Risk arising on account of lack of secondary market to provide ready exit options to the

investors/participants.

ii) Interest rate/currency risk: Mark to market risks arising on account of interest rate/currency fluctuations.

• Operational risk:

i) Co-mingling risk: Risk arising on account of comingling of funds belonging to investor(s) with that of

the originator and/or collection and processing servicer when there exist a time lag between collecting

amounts due from the obligors and payment made to the investors.

ii) Performance risk: Risk arising on account of the inability of a Collection and Processing Agent to collect

monies from the underlying obligors as well as operational difficulties in processing the payments.

iii) Regulatory and legal risk: Risk arising on account of

– non-compliance of the transaction structures with the extant applicable laws which may result in the

transaction(s) being rendered invalid;

– conflict between the provisions of the transaction documents with those of the underlying financial

facility agreements; and

– non-enforceability of security/claims due to imperfection in execution of the underlying facility

agreements with the borrower(s).

• Reputation risk: Risk arising on account of

i) rating downgrade of a securitised instrument due to unsatisfactory performance of the underlying asset

pool; and

ii) inappropriate practices followed by the collection and processing agent.

In addition to the above, securitised assets are exposed to prepayment and pipeline and warehousing risks.

Prepayment risk arises on account of prepayment of dues by obligors/borrowers in the assigned pool either in

part or full. Pipeline and warehousing risks refer to the event where originating banks are unable to off-load assets,

which were originated with an intention of selling thus potentially exposing them to losses arising on declining

values of these assets. The Bank does not follow the “originate to distribute” model and hence is not exposed to

the pipeline and warehousing risks.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2011