ICICI Bank 2011 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2011 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

Directed Lending

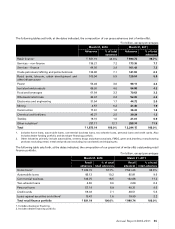

RBI requires banks to lend to certain sectors of the economy. Such directed lending comprises priority sector lending,

export credit and housing finance.

RBI guidelines require banks to lend 40.0% of their adjusted net bank credit, or credit equivalent amount of off-balance

sheet exposure, whichever is higher, to certain specified sectors called priority sectors. The definition of adjusted net

bank credit does not include certain exemptions and includes certain investments and is computed with reference to the

outstanding amount at March 31 of the previous year. Priority sector includes small enterprises, agricultural sector, food

and agri-based industries, small businesses and housing finance up to certain limits. Out of the 40.0%, banks are required

to lend a minimum of 18.0% of their adjusted net bank credit to the agriculture sector and the balance to certain specified

sectors, including small enterprises (defined as enterprises engaged in manufacturing/production, processing and

services businesses with a certain limit on investment in plant and machinery), small road and water transport operators,

small businesses, professional and self-employed persons, all other service enterprises, micro credit, education loans

and housing loans up to ` 2.0 million to individuals for purchase/construction of a dwelling unit per family.

In its letter dated April 26, 2002 granting its approval for the amalgamation of ICICI Limited and ICICI Bank Limited,

RBI stipulated that since the loans of erstwhile ICICI Limited (ICICI) transferred to us were not subject to the priority

sector lending requirement, we are required to maintain priority sector lending of 50.0% of our adjusted net bank

credit on the residual portion of our advances (i.e. the portion of our total advances excluding advances of ICICI at

year-end fiscal, 2002, referred to as “residual adjusted net bank credit”). This method of computation will apply until

such time as our aggregate priority sector advances reach a level of 40.0% of our adjusted net bank credit or review of

this stipulation by RBI. As required by RBI guidelines, we are also required to lend 10.0% of the residual adjusted net

bank credit or credit equivalent amount of off-balance sheet exposures, whichever is higher, to weaker sections. RBI’s

existing instructions on sub-targets under priority sector lending and eligibility of certain types of investments/funds

for qualification as priority sector advances apply to us.

We are required to comply with the priority sector lending requirements at the last ‘reporting Friday’ of each fiscal year.

The shortfall in the amount required to be lent to the priority sectors and weaker sections may be required to be

deposited with government sponsored Indian development banks like the National Bank for Agriculture and Rural

Development, the Small Industries Development Bank of India and the National Housing Bank. These deposits have

a maturity of up to seven years and carry interest rates lower than market rates. At year-end fiscal 2011, our total

investments in such bonds were ` 150.80 billion (including ` 21.34 billion of Bank of Rajasthan at August 12, 2010).

At March 25, 2011, the last reporting Friday for fiscal 2011, our priority sector loans were ` 551.73 billion, constituting

53.1% of our residual adjusted net bank credit against the requirement of 50.0%. At that date, qualifying agriculture

loans were 14.0% of our residual adjusted net bank credit as against the requirement of 18.0%. Our advances to

weaker sections were ` 34.43 billion constituting 3.3% of our residual adjusted net bank credit against the requirement

of 10.0%. The Bank has based its classifications of priority sector loans, including loans to weaker sections and

agriculture loans, in accordance with the guidelines and certain clarifications received from RBI during the year.

Classification of loans

We classify our assets as performing and non-performing in accordance with RBI guidelines. Under these guidelines,

an asset is classified as non-performing if any amount of interest or principal remains overdue for more than 90 days,

in respect of term loans. In respect of overdraft or cash credit, an asset is classified as non-performing if the account

remains out of order for a period of 90 days and in respect of bills, if the account remains overdue for more than 90

days. In compliance with regulations governing the presentation of financial information by banks, we report non-

performing assets net of cumulative write-offs in our financial statements.

RBI has separate guidelines for restructured loans. A fully secured standard asset can be restructured by re-

schedulement of principal repayments and/or the interest element, but must be separately disclosed as a restructured

asset. The diminution in the fair value of the loan, if any, measured in present value terms, is either written off or a

provision is made to the extent of the diminution involved. Similar guidelines apply to sub-standard loans. The sub-

standard or doubtful accounts which have been subject to restructuring, whether in respect of principal installment

or interest amount are eligible to be upgraded to the standard category only after the specified period, i.e., a period

of one year after the date when first payment of interest or of principal, whichever is earlier, falls due, subject to

satisfactory performance during the period.

Management’s Discussion & Analysis

66