ICICI Bank 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

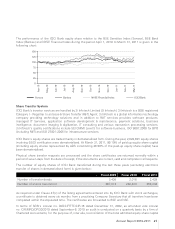

Business Overview

ECONOMIC OUTLOOK

The long-term fundamentals of the Indian economy continue to be strong. These include favourable demographics,

rising incomes, growing consuming class and a large investment pipeline. These growth drivers are expected to be

sustained over the medium-to-long term. The growth of the economy is being driven primarily by domestic investment

and consumption, with limited dependence on exports or the demand situation in other economies. In addition, the

growing economic activity in rural India and the emergence of smaller cities as important growth drivers are key

positive developments.

At the same time, there are some concerns, particularly with regard to inflation. Inflationary pressures emerging from

commodity and food prices have shown signs of becoming more generalised, leading to the containing of inflation

becoming the key priority of policy makers. In addition, the global economic environment continues to remain

uncertain with slow recovery and fiscal concerns in developed markets.

We believe that while these challenges may have an impact in the short term and cause periodic volatility, the strong

underlying fundamentals of the Indian economy would sustain high rates of growth over the medium to long term.

For a discussion of recent economic and regulatory developments, please refer to “Management’s Discussion &

Analysis”.

BUSINESS REVIEW

During fiscal 2011, the Bank focused on 5Cs strategy – Credit growth, CASA mobilisation, Cost optimization, Credit

quality improvement and Customer centricity. We believe that we have achieved substantial success on all the

parameters of this strategy and are well placed to leverage on the growth opportunities in the economy.

RETAIL BANKING

After significant moderation in previous years, retail credit growth in the system picked up pace in fiscal 2011. As per

data published by RBI for the period up to March 25, 2011, year-on-year retail credit growth was about 17%.

We continue to believe that retail credit in India has robust long-term growth potential, driven by sound fundamentals

of rising income levels and favorable demographic profile. We will continue to focus on select retail asset segments

like housing and vehicle loans where we expect significant demand over the medium to long term. We are also seeing

smaller markets beyond the large urban centres emerging as important drivers of growth in this segment. In addition,

customer segments are now maturing given the increase in incomes. These distinct customer segments, with widely

different requirements and risk-reward characteristics, require specialised strategies. We believe that our knowledge

of the customer and insights into the Indian market position us well to take advantage of these opportunities.

Our branches are the key points of customer acquisition and service. Accordingly, our organisation structure has

been shaped to provide greater empowerment to our branches. The branch network is expected to serve as an

integrated channel for deposit mobilisation, selected retail asset origination and distribution of third party products as

well as the focal point for customer service. The outbound sales teams have been strengthened and brought under

branch supervision. They are supported by the operations and phone banking teams to deliver high quality service,

customer retention and up-selling; and by a strategic product and service design team to design product and service

strategies for different customer segments. We have deepened our engagement and relationship with customers and

created more opportunities for cross-selling other products by introducing dedicated privilege banking areas, which

are manned by specially trained privilege bankers, and exclusive wealth branches for our high net worth customers.

The Bank’s focus during the year was on delivering superior customer service in line with its articulated Khayaal Aapka

proposition.

During the year, we acquired The Bank of Rajasthan which substantially enhanced our branch network and strengthened

our presence in northern and western India. The merger of Bank of Rajasthan added over 450 branches to our network.

Including these, our branch network has increased from 1,707 branches at March 31, 2010 to 2,529 branches at March 31,

2011. We also increased our ATM network from 5,219 ATMs at March 31, 2010 to 6,055 ATMs at March 31, 2011.

34