ICICI Bank 2011 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2011 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

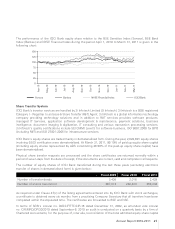

During fiscal 2011, we continued our focus on increasing the proportion of low-cost retail deposits in our funding base.

Our current and savings account (CASA) deposits as a percentage of total deposits increased from 41.7% at March

31, 2010 to 45.1% at March 31, 2011.

During the year, our retail disbursements increased as we focused on opportunities in residential mortgages, vehicle

finance and construction equipment finance. The realignment of our retail sales and service architecture helped

us increase our reach while simultaneously bringing focus towards customer service. We sourced an increasing

proportion of our mortgage business through our branch network. In addition to mortgages, we also saw traction in

auto loans, commercial vehicle financing and construction equipment business in fiscal 2011.

We also continued to focus on cross-selling new products and products of our life and general insurance subsidiaries

to our existing customers. Cross-sell allows us to deepen our relationship with our existing customers and earn fee

income. We will continue to focus on cross-sell as a means to improve profitability and offer a complete suite of

products to our customers.

SMALL ENTERPRISES

Medium & small enterprises are important engines of growth and reflect India’s entrepreneurial energy. We offer

complete banking solutions to small and medium enterprises across industry segments. We support the growth of

the small and medium enterprises sector while adopting a cluster based financing approach for enterprises with a

homogeneous profile in industries such as infrastructure, engineering, information technology, education, life-sciences

and agri-based businesses. We also offer supply chain financing solutions to the channel partners of large corporates.

During fiscal 2011, we strengthened the sales and relationship coverage by increasing our presence with greater

empowerment at zonal levels. This has allowed us to deepen our customer relationships and supplement the customer

acquisition by leveraging our branch network along with our commercial banking franchise. The Bank also contributes

significantly to the SME eco-system through multiple initiatives such SME CEOs Knowledge Series, Emerging India

Awards, SME Expos and the SME Toolkit - an online business and advisory resource.

We have a long tradition of partnering entrepreneurs early in their growth phase, building lasting and mutually beneficial

relationships that deliver recurring value. We will continue to further strengthen our proposition and penetration in this

segment.

CORPORATE BANKING

Our corporate banking strategy is based on providing comprehensive and customised financial solutions to our

corporate customers. We offer a comprehensive suite of corporate banking products including rupee and foreign

currency debt, working capital credit, structured financing, loan syndication and commercial banking products and

services. Our corporate and investment banking franchise is built around a core relationship team that has strong

relationships with almost all of the country’s corporate houses. The relationship team is product agnostic and is

responsible for managing banking relationships with clients. We have also put in place product specific teams with

a view to focus on designing financial solutions for clients spread across structured finance, project finance, loan

syndication and markets. The Structured Finance Group is responsible for working with the relationship team in India

and our international subsidiaries and branches for structuring and execution of investment banking mandates and

other transactions.

We have a Commercial Banking Group working closely with the Corporate Banking Group for growing this business

through identified branches. Our strategy for growth in commercial banking, i.e. of meeting the regular banking

requirements of companies for transactions and trade, is based on leveraging our strong client relationships and

focusing on enhancing client servicing capability at the operational level.

We have enhanced our client servicing capability by the effective use of “Mega Branches” spread across all major

commercial centres across the country catering to specialised commercial banking needs of clients. These branches

have highly cohesive and dedicated customer focused transaction teams, led by senior branch heads, to service

customers and provide a better transactional experience to the client. An efficient central operations team complements

the service delivery capability.

Annual Report 2010-2011 35