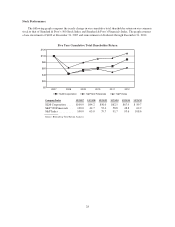

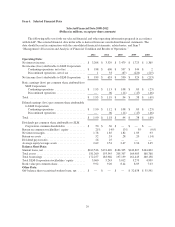

Sallie Mae 2012 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

Provisions for Loan Losses

Management estimates and maintains an allowance for loan losses at a level sufficient to cover charge-offs

expected over the next two years, plus an additional allowance to cover life-of-loan expected losses for loans

classified as a troubled debt restructuring (“TDR”). The provision for loan losses increases the related allowance

for loan losses. Generally, the allowance for loan losses rises when charge-offs are expected to increase and falls

when charge-offs are expected to decline. Our loss exposure and resulting provision for losses is small for

FFELP Loans because we generally bear a maximum of three percent loss exposure on them. We bear the full

credit exposure on our Private Education Loans. Our provision for losses in our FFELP Loans segment was

$72 million in 2012 compared with $86 million in 2011. Losses in our Consumer Lending segment are

determined by risk characteristics such as school type, loan status (in-school, grace, forbearance, repayment and

delinquency), loan seasoning (number of months in active repayment), underwriting criteria (e.g., credit scores),

a cosigner and the current economic environment. Our provision for loan losses in our Consumer Lending

segment was $1.0 billion in 2012 compared with $1.2 billion in 2011.

Charge-Offs and Delinquencies

When we conclude a loan is uncollectible, the unrecoverable portion of the loan is charged against the

allowance for loan losses in the applicable segment. Charge-off data provides relevant information with respect

to the performance of our loan portfolios. Management focuses on delinquencies as well as the progression of

loans from early to late stage delinquency. The Consumer Lending segment’s charge-off rate was 3.37 percent of

loans in repayment in 2012 compared with 3.72 percent of loans in repayment in 2011. Delinquencies are a very

important indicator of the potential future credit performance. Private Education Loan delinquencies as a

percentage of Private Education Loans in repayment decreased from 10.1 percent at December 31, 2011 to

9.3 percent at December 31, 2012.

Servicing and Contingency Revenues

We earn servicing revenues from servicing student loans, Campus Solutions, and from account asset

servicing related to 529 college-savings plans. We earn contingency revenue related to default aversion and

contingency collections work we perform primarily on federal loans. The fees we recognize are primarily driven

by our success in collecting or rehabilitating defaulted loans, the number of transactions processed and the

underlying volume of loans we are servicing on behalf of others.

Other Income / (Loss)

In managing our loan portfolios and funding sources we periodically engage in sales of loans and the

repurchase of our outstanding debt. In each case, depending on market conditions, we may incur gains or losses

from these transactions that affect our results from operations.

Operating Expenses

The operating expenses reported for our Consumer Lending and Business Services segments are those that

are directly attributable to the generation of revenues by those segments. The operating expenses for the FFELP

Loans segment primarily represent an intercompany servicing charge from the Business Services segment and do

not reflect our actual underlying costs incurred to service the loans. We have included corporate overhead

expenses and certain information technology costs (together referred to as “Overhead”) in our Other segment

rather than allocate those expenses by segment. Overhead expenses include executive management, the board of

directors, accounting, finance, legal, human resources, stock-based compensation expense and certain

information technology and infrastructure costs.

32