Sallie Mae 2012 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

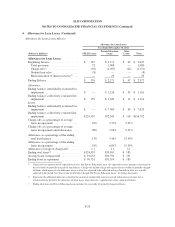

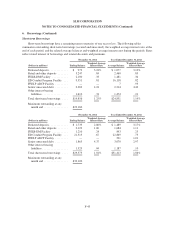

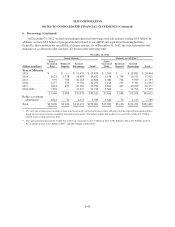

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

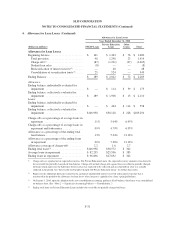

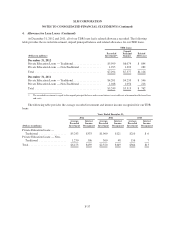

4. Allowance for Loan Losses (Continued)

Private Education Non-Traditional Loan

Delinquencies

December 31,

2012 2011 2010

(Dollars in millions) Balance % Balance % Balance %

Loans in-school/grace/deferment(1) ........................ $ 483 $ 656 $ 921

Loans in forbearance(2) ................................. 140 191 184

Loans in repayment and percentage of each status:

Loans current ....................................... 1,978 76.5% 2,012 74.0% 2,038 72.6%

Loans delinquent 31-60 days(3) ......................... 175 6.8 208 7.7 217 7.7

Loans delinquent 61-90 days(3) ......................... 106 4.1 127 4.7 131 4.7

Loans delinquent greater than 90 days(3) .................. 325 12.6 371 13.6 422 15.0

Total non-traditional loans in repayment ................. 2,584 100% 2,718 100% 2,808 100%

Total non-traditional loans, gross ......................... 3,207 3,565 3,913

Non-traditional loans unamortized discount ................. (83) (81) (93)

Total non-traditional loans .............................. 3,124 3,484 3,820

Non-traditional loans receivable for partially charged-off

loans ............................................. 550 536 482

Non-traditional loans allowance for losses .................. (534) (629) (791)

Non-traditional loans, net ............................... $3,140 $3,391 $3,511

Percentage of non-traditional loans in repayment ............. 80.6% 76.2% 71.8%

Delinquencies as a percentage of non-traditional loans in

repayment ......................................... 23.4% 26.0% 27.4%

Loans in forbearance as a percentage of loans in repayment and

forbearance ........................................ 5.1% 6.6% 6.1%

(1) Deferment includes customers who have returned to school or are engaged in other permitted educational activities and are not yet

required to make payments on the loans, e.g., residency periods for medical students or a grace period for bar exam preparation.

(2) Loans for customers who have requested extension of grace period generally during employment transition or who have temporarily

ceased making full payments due to hardship or other factors, consistent with established loan program servicing policies and procedures.

(3) The period of delinquency is based on the number of days scheduled payments are contractually past due.

Receivable for Partially Charged-Off Private Education Loans

At the end of each month, for loans that are 212 days past due, we charge off the estimated loss of a

defaulted loan balance. Actual recoveries are applied against the remaining loan balance that was not charged off.

We refer to this remaining loan balance as the “receivable for partially charged-off loans.” If actual periodic

recoveries are less than expected, the difference is immediately charged off through the allowance for loan losses

with an offsetting reduction in the receivable for partially charged-off Private Education Loans. If actual periodic

recoveries are greater than expected, they will be reflected as a recovery through the allowance for Private

Education Loan losses once the cumulative recovery amount exceeds the cumulative amount originally expected

to be recovered. Private Education Loans which defaulted between 2008 and 2011 for which we have previously

charged off estimated losses have, to varying degrees, not met our post-default recovery expectations to date and

may continue not to do so. According to our policy, we have been charging off these periodic shortfalls in

expected recoveries against our allowance for Private Education Loan losses and the related receivable for

F-35