Sallie Mae 2012 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

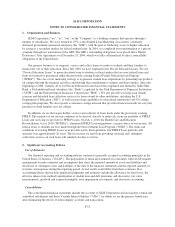

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. Significant Accounting Policies (Continued)

Securitization Accounting

Our securitizations use a two-step structure with a special purpose entity that legally isolates the transferred

assets from us, even in the event of bankruptcy. Transactions receiving sale treatment are also structured to

ensure that the holders of the beneficial interests issued are not constrained from pledging or exchanging their

interests, and that we do not maintain effective control over the transferred assets. If these criteria are not met,

then the transaction is accounted for as an on-balance sheet secured borrowing. In all cases, irrespective of

whether they qualify as accounting sales our securitizations are legally structured to be sales of assets that isolate

the transferred assets from us. If a securitization qualifies as a sale, we then assess whether we are the primary

beneficiary of the securitization trust and are required to consolidate such trust. (See “Consolidation” of this

Note 2.) If we are the primary beneficiary then no gain or loss is recognized. See “Consolidation” of this Note 2

for additional information regarding the accounting rules for consolidation when we are the primary beneficiary

of these trusts.

Irrespective of whether a securitization receives sale or on-balance sheet treatment, our continuing

involvement with our securitization trusts is generally limited to:

• Owning the equity certificates of certain trusts.

• The servicing of the student loan assets within the securitization trusts, on both a pre- and post-default

basis.

• Our acting as administrator for the securitization transactions we sponsored, which includes

remarketing certain bonds at future dates.

• Our responsibilities relative to representation and warranty violations.

• Temporarily advancing to the trust certain borrower benefits afforded the borrowers of student loans

that have been securitized. These advances subsequently are returned to us in the next quarter.

• Certain back-to-back derivatives entered into by us contemporaneously with the execution of

derivatives by certain Private Education Loan securitization trusts.

• The option held by us to buy certain delinquent loans from certain Private Education Loan

securitization trusts.

• The option to exercise the clean-up call and purchase the student loans from the trust when the asset

balance is 10 percent or less of the original loan balance.

• The option (in certain trusts) to call rate reset notes in instances where the remarketing process has

failed.

• The option (in certain trusts that were TALF eligible in 2009) to call the outstanding bonds at a

discount to par at a future date

The investors of the securitization trusts have no recourse to our other assets should there be a failure of the

trusts to pay when due. Generally, the only arrangements under which we have to provide financial support to the

trusts are representation and warranty violations requiring the buyback of loans.

Under the terms of the transaction documents of certain trusts, we have, from time to time, exercised our

options to purchase delinquent loans from Private Education Loan trusts, to purchase the remaining loans from

trusts once the loan balance falls below 10 percent of the original amount, or to call rate reset notes. Certain trusts

maintain financial arrangements with third parties also typical of securitization transactions, such as derivative

contracts (swaps) and bond insurance policies that, in the case of a counterparty failure, could adversely impact

the value of any Residual Interest.

F-20