Sallie Mae 2012 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

|

|

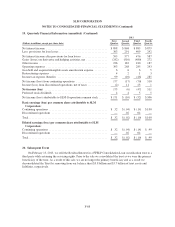

SLM CORPORATION

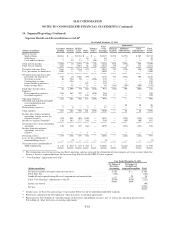

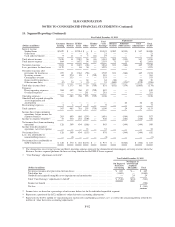

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

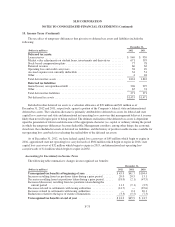

17. Discontinued Operations (Continued)

The Purchased Paper — Mortgage/Properties business and the Purchased Paper — Non-Mortgage business

comprise operations and cash flows that can be clearly distinguished operationally and for financial reporting

purposes, from the rest of the Company. Accordingly, this Component is presented as discontinued operations as

(1) the operations and cash flows of the Component have been eliminated from our ongoing operations as of

December 31, 2010, and (2) we will have no continuing involvement in the operations of this Component

subsequent to the sale of the Purchased Paper-Non Mortgage business.

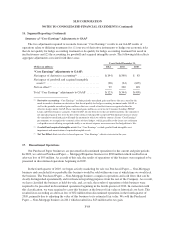

The following table summarizes the discontinued operations.

Years Ended December 31,

(Dollars in millions) 2012 2011 2010

Operations:

Income (loss) from discontinued operations before income taxes . . $ 1 $53 $(91)

Income tax expense (benefit) .............................. — 20 (24)

Income (loss) from discontinued operations, net of taxes ........ $ 1 $33 $(67)

18. Concentrations of Risk

Our business is primarily focused in providing and/or servicing to help students and their families save, plan

and pay for college. We primarily originate, service and/or collect loans made to students and their families to

finance the cost of their education. We provide funding, delivery and servicing support for education loans in the

United States, through our Private Education Loan programs and as a servicer and collector of loans for ED. In

addition we are the largest holder, servicer and collector of loans under the discontinued FFELP. Because of this

concentration in one industry, we are exposed to credit, legislative, operational, regulatory, and liquidity risks

associated with the student loan industry.

Concentration Risk in the Revenues Associated with Private Education Loans

We compete in the private credit lending business with banks and other consumer lending institutions, many

with strong consumer brand name recognition and greater financial resources. We compete based on our

products, origination capability and customer service. To the extent our competitors compete aggressively or

more effectively, we could lose market share to them or subject our existing loans to refinancing risk. Our

product offerings may not prove to be profitable and may result in higher than expected losses.

We are a leading provider of saving- and paying-for-college products and programs. This concentration

gives us a competitive advantage in the marketplace. This concentration also creates risks in our business,

particularly in light of our concentrations as a Private Education Loan lender and as a servicer for the FFELP and

DSLP. If population demographics result in a decrease in college-age individuals, if demand for higher education

decreases, if the cost of attendance of higher education decreases, if public resistance to higher education costs

increases, or if the demand for higher education loans decreases, our consumer lending business could be

negatively affected. In addition, the federal government, through the DSLP, poses significant competition to our

private credit loan products. If loan limits under the DSLP increase, DSLP loans could be more widely available

to students and their families and DSLP loans could increase, resulting in further decreases in the size of the

Private Education Loan market and demand for our Private Education Loan products.

F-85