Sallie Mae 2012 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207

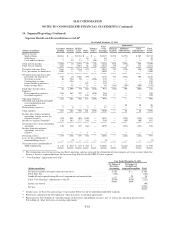

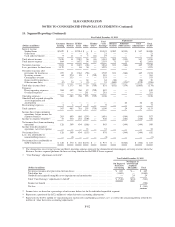

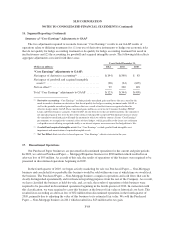

|

|

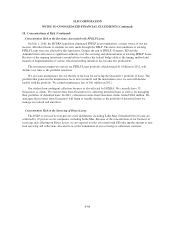

On December 23, 2011, the President signed the Consolidated Appropriations Act of 2012 into law. This law

includes changes that permit FFELP lenders or beneficial holders to change the index on which the Special

Allowance Payments are calculated for FFELP Loans first disbursed on or after January 1, 2000. The law allows

holders to elect to move the index from the Commercial Paper (“CP”) Rate to the one-month London Inter Bank

Offered Rate (“LIBOR”). Such elections have been made by April 1, 2012.

Eligible Lenders, Students and Educational Institutions

Lenders who were eligible to make loans under the FFELP generally included banks, savings and loan

associations, credit unions, pension funds and, under some conditions, schools and guaranty agencies. FFELP

Loans were made to, or on behalf of, a “qualified student.” A “qualified student” is an individual who

• is a United States citizen, national or permanent resident;

• has been accepted for enrollment or is enrolled and maintaining satisfactory academic progress at a

participating educational institution; and

• is carrying at least one-half of the normal full-time academic workload for the course of study the student is

pursuing.

A student qualified for a subsidized Stafford Loan if his family met the financial need requirements for the

particular loan program. Only PLUS Loan borrowers have to meet credit standards.

Eligible schools included institutions of higher education, including proprietary institutions, meeting the

standards provided in the HEA. For a school to participate in the program, the U.S. Department of Education

(“ED”) had to approve its eligibility under standards established by regulation.

Financial Need Analysis

Subject to program limits and conditions, student loans generally were made in amounts sufficient to cover the

student’s estimated costs of attending school, including tuition and fees, books, supplies, room and board,

transportation and miscellaneous personal expenses as determined by the institution. Generally, each loan

applicant (and parents in the case of a dependent child) underwent a financial need analysis.

Special Allowance Payments (“SAP”)

The HEA provides for quarterly Special Allowance Payments to be made by ED to holders of student loans to

the extent necessary to ensure that they receive at least specified market interest rates of return. The rates for

Special Allowance Payments depend on formulas that vary according to the type of loan, the date the loan was

made and the type of funds, tax-exempt or taxable, used to finance the loan. ED makes a Special Allowance

Payment for each calendar quarter.

The Special Allowance Payment equals the average unpaid principal balance, including interest which has

been capitalized, of all eligible loans held by a holder during the quarterly period multiplied by the special

allowance percentage.

For a discussion on the computation of the special allowance percentage and special allowance margin, see

Appendix A to our 2010 Form 10-K.

Fees

Loan Rebate Fee. A loan rebate fee of 1.05% is paid annually on the unpaid principal and interest of each

Consolidation Loan disbursed on or after October 1, 1993. This fee was reduced to .62% for loans made from

October 1, 1998 to January 31, 1999.

A-2