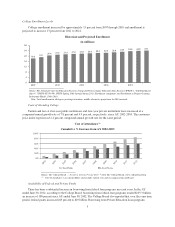

Sallie Mae 2012 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

Regulation of Systemically Important Non-Bank Financial Companies. As directed by the Dodd-Frank Act, on

April 3, 2012, the Financial Stability Oversight Council (“FSOC”) approved the final rule and interpretive guidance

it will use for designating non-bank financial companies as systemically important to the financial stability of the

United States and subject to supervision by the Board of Governors of the Federal Reserve System (the “FRB”)

under enhanced prudential supervision and regulatory standards. To be subject to FRB enhanced supervision, a non-

bank financial company’s material financial distress, its nature, scope, size, scale, concentration, interconnectedness,

or mix of activities, must pose a threat to the financial stability of the United States. For a further discussion of the

risks and implications of SLM Corporation being designated a Systematically Important Financial Institution

(“SIFI”), see Item 1A “Risk Factors — Legal, Regulatory and Compliance.”

The FSOC’s process for determining if a non-bank financial company’s distress could pose a threat to the

financial stability of the United States focuses on three criteria: the size, substitutability and interconnectedness

of the particular company. In the final rule, the FSOC provided guidance on the process they would use for

determining the SIFI designation. In Stage 1 of the process, the FSOC uses quantitative criteria to determine

which non-bank financial companies would be subject to a Stage 2 review, during which the FSOC conducts a

quantitative and qualitative review of publicly available information to determine whether there is a likelihood a

company could be a SIFI and meriting further review of the company’s nonpublic information. Under Stage 3 of

the process, the FSOC notifies the company and works with it to review additional information that may not be

available publicly and determines whether to make an official designation.

In the last quarter of 2012, the FSOC advanced several large non-bank financial companies to Stage 3 of the

process. SLM Corporation was not one of these companies. At the same time, the FSOC affirmatively decided

not to advance other Stage 2 non-bank financial companies to Stage 3 of the process.

While we have no way of knowing the qualitative judgments the FSOC will use in the future to determine if

SLM Corporation merits SIFI designation, and no assurances can be given, we continue to believe it is unlikely

the FSOC will determine SLM Corporation poses a threat to the financial stability of the United States. While

SLM Corporation meets certain criteria in Stage 1 of the FSOC’s rule, we see no changes that would warrant the

FSOC to consider us for SIFI designation due to the nature of the majority of financial assets on our balance

sheet, the minimal interconnectivity between our businesses and the financial economy of the United States or

the numerous sophisticated competitors who can provide substitute services to those we provide.

Oversight of Derivatives. The Dodd-Frank Act created a comprehensive new regulatory framework for

derivatives transactions, to be implemented by the Commodity Futures Trading Commission (the “CFTC”) and

the SEC. This new framework, among other things, subjects certain swap participants to new capital and margin

requirements, recordkeeping and business conduct standards and imposes registration and regulation of swap

dealers and major swap participants. The scope of potential exemptions remains to be further defined through

agency rulemakings. Moreover, while we may or may not qualify for exemptions, many of our derivatives

counterparties are likely to be subject to the new capital, margin and business conduct requirements.

Other Significant Sources of Regulation

Many aspects of our businesses are subject to regulation by federal and state regulation and administrative

oversight. Some of the most significant of these are described below.

We are subject to the HEA and, from time to time, our student loan operations are reviewed by ED and

Guarantors. As a servicer of federal student loans, we are subject to certain ED regulations regarding financial

responsibility and administrative capability that govern all third-party servicers of insured student loans. In

connection with our Guarantor servicing operations, we must comply with, on behalf of our Guarantor clients,

certain ED regulations that govern Guarantor activities as well as agreements for reimbursement between ED and

our Guarantor clients.

As a third-party service provider to financial institutions, we are also subject to examination by the Federal

Financial Institutions Examination Council (“FFIEC”). The Bank is subject to Utah banking regulations as well

13