Sallie Mae 2012 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

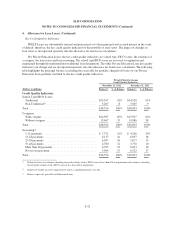

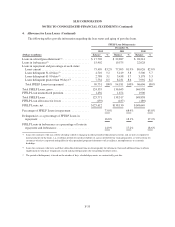

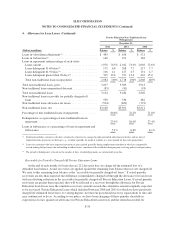

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. Significant Accounting Policies (Continued)

allocated to common shareholders by the weighted average common shares outstanding plus amounts

representing the dilutive effect of stock options outstanding, restricted stock, restricted stock units, and the

outstanding commitment to issue shares under the Employee Stock Purchase Plan. See “Note 10—Earnings

(Loss) per Common Share” for further discussion.

Discontinued Operations

A “Component” of a business comprises operations and cash flows that can be clearly distinguished

operationally and for financial reporting purposes from the rest of the Company. When we determine that a

Component of our business has been disposed of or has met the criteria to be classified as held-for-sale such

Component is presented separately as discontinued operations if the operations of the Component have been or

will be eliminated from our ongoing operations and we will have no continuing involvement with the Component

after the disposal transaction is complete. See “Note 17—Discontinued Operations” for further discussion. If a

component is classified as held-for-sale, then it is carried at the lower of its cost basis or fair value. Included

within discontinued operations are the accounting results related to our purchasing delinquent and charged-off

receivables on various types of consumer debt with a primary emphasis on charged-off credit card receivables,

and sub-performing and non-performing mortgage loans (Purchased Paper businesses). At December 31, 2012,

we have sold all of these businesses.

Statement of Cash Flows

Included in our financial statements is the consolidated statement of cash flows. It is our policy to include

all derivative net settlements, irrespective of whether the derivative is a qualifying hedge, in the same section of

the statement of cash flows that the derivative is economically hedging.

As discussed in “Restricted Cash and Investments” of this Note 2, our restricted cash balances primarily

relate to on-balance sheet securitizations. This balance is primarily the result of timing differences between when

principal and interest is collected on the trust assets and when principal and interest is paid on the trust liabilities.

As such, changes in this balance are reflected in investing activities.

Reclassifications

Certain reclassifications have been made to the balances as of and for the years ended December 31, 2011

and 2010, to be consistent with classifications adopted for 2012, which had no effect on net income, total assets

or total liabilities.

3. Student Loans

There are three principal categories of FFELP Loans: Stafford, PLUS, and FFELP Consolidation Loans.

Generally, Stafford and PLUS Loans have repayment periods of between five and ten years. FFELP

Consolidation Loans have repayment periods of twelve to thirty years. FFELP Loans do not require repayment,

or have modified repayment plans, while the customer is in-school and during the grace period immediately upon

leaving school. The customer may also be granted a deferment or forbearance for a period of time based on need,

during which time the customer is not considered to be in repayment. Interest continues to accrue on loans in the

in-school, deferment and forbearance period. FFELP Loans obligate the customer to pay interest at a stated fixed

rate or a variable rate reset annually (subject to a cap) on July 1 of each year depending on when the loan was

originated and the loan type. FFELP Loans disbursed before April 1, 2006 earn interest at the greater of the

F-25