Sallie Mae 2012 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2012 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

|

|

SLM CORPORATION

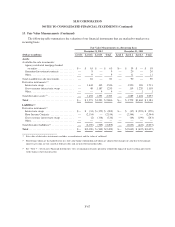

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

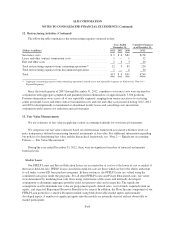

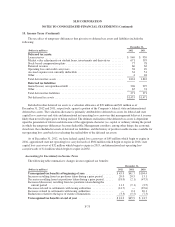

13. Fair Value Measurements (Continued)

The following table presents the significant inputs that are unobservable or from inactive markets used in

the recurring valuations of the level 3 financial instruments detailed above.

(Dollars in millions)

Fair Value at

December 31, 2012

Valuation

Technique Input

Range

(Weighted Average)

Derivatives

Consumer Price Index/LIBOR

basis swaps .............. $ 92 Discounted cash flow

Bid/ask adjustment

to discount rate

0.02% — 0.04%

(0.05%)

Prime/LIBOR basis swaps .... (165) Discounted cash flow Constant prepayment rate 4.3%

Bid/ask adjustment to

discount rate

0.08% — 0.08%

(0.08%)

Cross-currency interest rate

swaps ................... 1,053 Discounted cash flow Constant prepayment rate 2.6%

Other ..................... 4

Total ..................... $ 984

The significant inputs that are unobservable or from inactive markets related to our level 3 derivatives

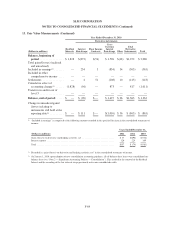

detailed in the table above would be expected to have the following impacts to the valuations:

• Consumer Price Index/LIBOR basis swaps — These swaps do not actively trade in the markets as

indicated by a wide bid/ask spread. A wider bid/ask spread will result in a decrease in the overall

valuation.

• Prime/LIBOR basis swaps — These swaps do not actively trade in the markets as indicated by a wide

bid/ask spread. A wider bid/ask spread will result in a decrease in the overall valuation. In addition, the

unobservable inputs include constant prepayment rates of the underlying securitization trust the swap

references. A decrease in this input will result in a longer weighted average life of the swap which will

increase the value for swaps in a gain position and decrease the value for swaps in a loss position,

everything else equal. The opposite is true for an increase in the input.

• Cross-currency interest rate swaps — The unobservable inputs used in these valuations are constant

prepayment rates of the underlying securitization trust the swap references. A decrease in this input

will result in a longer weighted average life of the swap. All else equal in a typical currency market,

this will result in a decrease to the valuation due to the delay in the cash flows of the currency

exchanges as well as diminished liquidity in the forward exchange markets as you increase the term.

The opposite is true for an increase in the input.

F-70