IBM 2010 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2010 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

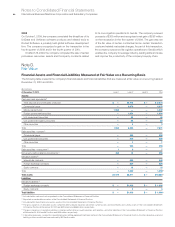

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies96

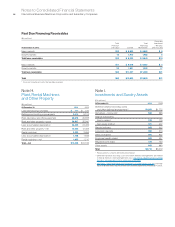

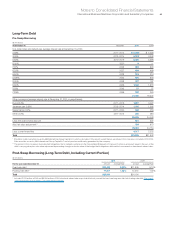

Pre-swap annual contractual maturities of long-term debt out-

standing at December 31, 2010, are as follows:

($ in millions)

2011 $ 4,021

2012 4,209

2013 5,451

2014 1,329

2015 168

2016 and beyond 10,427

To t a l $25,606

Interest on Debt

($ in millions)

For the year ended December 31: 2010 2009 2008

Cost of financing $555 $ 706 $ 788

Interest expense 365 404 687

Net investment derivative activity 3 (1) (13)

Interest capitalized 5 13 15

Total interest paid and accrued $928 $1,122 $1,477

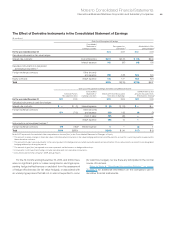

Refer to the related discussion on page 128 in note V, “Seg ment

Infor mation,” for total interest expense of the Global Financing

segment. See note L, “Derivative Financial Instruments,” on pages

96 through 101 for a discussion of the use of currency and interest

rate swaps in the company’s debt risk management program.

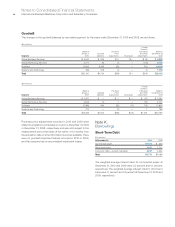

Lines of Credit

The company maintains a five-year, $10 billion Credit Agreement

(the “Credit Agreement”), which expires on June 28, 2012. The total

expense recorded by the company related to this facility was $6.2

million in 2010, $6.3 million in 2009 and $6.2 million in 2008. The

Credit Agreement permits the company and its Subsidiary Borrowers

to borrow up to $10 billion on a revolving basis. Borrowings of the

Subsidiary Borrowers will be unconditionally backed by the com-

pany. The company may also, upon the agreement of either existing

lenders, or of the additional banks not currently party to the Credit

Agreement, increase the commitments under the Credit Agreement

up to an additional $2.0 billion. Subject to certain terms of the Credit

Agreement, the company and Subsidiary Borrowers may borrow,

prepay and reborrow amounts under the Credit Agreement at any

time during the Credit Agreement. Interest rates on borrowings under

the Credit Agreement will be based on prevailing market interest

rates, as further described in the Credit Agreement. The Credit

Agreement contains customary representations and warranties,

covenants, events of default, and indemnification provisions. The

company believes that circumstances that might give rise to breach

of these covenants or an event of default, as specified in the Credit

Agreement, are remote. The company’s other lines of credit, most

of which are uncommitted, totaled approximately $14,679 million

and $9,790 million at December 31, 2010 and 2009, respectively.

Interest rates and other terms of borrowing under these lines of credit

vary from country to country, depending on local market conditions.

($ in millions)

At December 31: 2010 2009

Unused lines:

From the committed global credit facility $ 9,926 $ 9,910

From other committed and uncommitted lines 11,462 7,405

Total unused lines of credit $21,388 $17,314

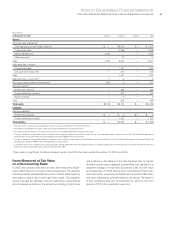

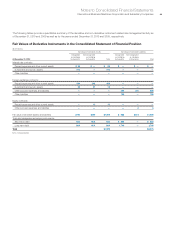

Note L.

Derivative Financial Instruments

The company operates in multiple functional currencies and is

a significant lender and borrower in the global markets. In the

normal course of business, the company is exposed to the impact

of interest rate changes and foreign currency fluctuations, and to

a lesser extent equity and commodity price changes and client

credit risk. The company limits these risks by following established

risk management policies and procedures, including the use

of derivatives, and, where cost effective, financing with debt in

the currencies in which assets are denominated. For interest rate

exposures, derivatives are used to better align rate movements

between the interest rates associated with the company’s lease

and other financial assets and the interest rates associated with

its financing debt. Derivatives are also used to manage the related

cost of debt. For foreign currency exposures, derivatives are used

to better manage the cash flow volatility arising from foreign

exchange rate fluctuations.

As a result of the use of derivative instruments, the company

is exposed to the risk that counterparties to derivative contracts

will fail to meet their contractual obligations. To mitigate the

counterparty credit risk, the company has a policy of only entering

into contracts with carefully selected major financial institutions

based upon their credit ratings and other factors. The company’s

established policies and procedures for mitigating credit risk on

principal transactions include reviewing and establishing limits for

credit exposure and continually assessing the creditworthiness

of counterparties. The right of set-off that exists under certain of

these arrangements enables the legal entities of the company

subject to the arrangement to net amounts due to and from the

counterparty reducing the maximum loss from credit risk in the

event of counterparty default.

The company is also a party to collateral security arrangements

with most of its major counterparties. These arrangements require

the company to hold or post collateral (cash or U.S. Treasury

securities) when the derivative fair values exceed contractually

established thresholds. Posting thresholds can be fixed or can

vary based on credit default swap pricing or credit ratings received

from the major credit agencies. The aggregate fair value of all

derivative instruments under these collateralized arrangements

that were in a liability position at December 31, 2010 and 2009

was $363 million and $779 million, respectively, for which the com-

pany has posted collateral of $9 million and $37 million, respec-

tively. Full collateralization of these agreements would be required

in the event that the company’s credit rating falls below investment

grade or if its credit default swap spread exceeds 250 basis points,

as applicable, pursuant to the terms of the collateral security