IBM 2010 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2010 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

49

Management Discussion

International Business Machines Corporation and Subsidiary Companies

Total contractual obligations are reported in the table above exclud-

ing the effects of time value and therefore, may not equal the amounts

reported in the Consolidated Statement of Financial Position.

Purchase obligations include all commitments to purchase goods

or services of either a fixed or minimum quantity that meet any of

the following criteria: (1) they are noncancelable, (2) the company

would incur a penalty if the agreement was canceled, or (3) the

company must make specified minimum payments even if it does

not take delivery of the contracted products or services (take-or-pay).

If the obligation to purchase goods or services is noncancelable, the

entire value of the contract is included in the table above. If the

obligation is cancelable, but the company would incur a penalty if

canceled, the dollar amount of the penalty is included as a purchase

Events that could temporarily change the historical cash flow

dynamics discussed earlier include significant changes in operating

results, material changes in geographic sources of cash, unexpected

adverse impacts from litigation, future pension funding requirements

during periods of severe downturn in the capital markets or the

timing of tax payments. Whether any litigation has such an adverse

impact will depend on a number of variables, which are more com-

pletely described in note O, “Contingencies and Commitments,” on

pages 103 through 105. With respect to pension funding, in 2010,

the company contributed $865 million to its non-U.S. defined ben-

efit plans, versus $1,252 million in 2009. As highlighted in the

Contractual Obligations table below, the company expects to make

legally mandated pension plan contributions to certain non-U.S.

obligation. Contracted minimum amounts specified in take-or-pay

contracts are also included in the table as they represent the portion

of each contract that is a firm commitment.

In the ordinary course of business, the company enters into con-

tracts that specify that the company will purchase all or a portion of

its requirements of a specific product, commodity or service from a

supplier or vendor. These contracts are generally entered into in order

to secure pricing or other negotiated terms. They do not specify fixed

or minimum quantities to be purchased and, therefore, the company

does not consider them to be purchase obligations.

Interest on floating rate debt obligations is calculated using the

effective interest rate at December 31, 2010, plus the interest rate

spread associated with that debt, if any.

plans of approximately $3.9 billion in the next five years. The 2011

contributions are currently expected to be approximately $900

million. Financial market performance in 2011 could increase the

legally mandated minimum contributions in certain non-U.S. coun-

tries that require more frequent remeasurement of the funded

status. The company is not quantifying any further impact from

pension funding because it is not possible to predict future move-

ments in the capital markets or pension plan funding regulations.

The Pension Protection Act of 2006 was enacted into law in

2006, and, among other things, increases the funding requirements

for certain U.S. defined benefit plans beginning after December

31, 2007. No mandatory contribution is required for the U.S. defined

benefit plan in 2011 as of December 31, 2010.

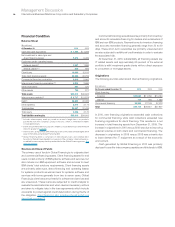

Contractual Obligations

($ in millions)

To t a l

Contractual Payments due in

Payment Stream 2011 2012–13 2014–15 After 2015

Long-term debt obligations $25,493 $3,996 $ 9,594 $1,482 $10,422

Interest on long-term debt obligations 11,902 1,577 2,046 1,350 6,931

Capital (finance) lease obligations 111 25 66 16 5

Operating lease obligations 5,510 1,521 2,101 1,250 638

Purchase obligations 1,547 646 562 285 54

Other long-term liabilities:

Minimum pension funding (mandated)* 3,900 900 1,600 1,400 —

Executive compensation 1,350 70 157 179 945

Long-term termination benefits 1,503 141 263 221 879

Tax reserves** 3,441 280 — — —

Other 1,184 39 83 71 992

Tot a l $55,943 $9,194 $16,470 $6,252 $20,866

* Represents future pension contributions that are mandated by local regulations or statute, all associated with non-U.S. qualified pension plans. See note U, “Retirement-Related

Benefits,” on pages 112 to 126 for additional information on the non-U.S. plans’ investment strategies and expected contributions and for information regarding the company’s total

underfunded pension plans of $16,804 million at December 31, 2010. As the funded status on the plans will vary, obligations for mandated minimum pension payments after

2015 could not be reasonably estimated.

** These amounts represent the liability for unrecognized tax benefits. The company estimates that approximately $280 million of the liability is expected to be settled within the

next 12 months. The settlement period for the noncurrent portion of the income tax liability cannot be reasonably estimated as the timing of the payments will depend on the

progress of tax examinations with the various tax authorities; however, it is not expected to be due within the next 12 months.