IBM 2010 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2010 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

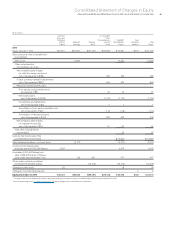

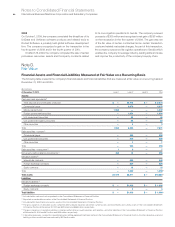

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies 77

In determining the fair value of financial instruments, the com-

pany considers certain market valuation adjustments to the “base

valuations” calculated using the methodologies described below

for several parameters that market participants would consider in

determining fair value:

•

Counterparty credit risk adjustments are applied to financial

instru ments, taking into account the actual credit risk of a coun-

terparty as observed in the credit default swap market to

determine the true fair value of such an instrument.

• Credit risk adjustments are applied to reflect the company’s

own credit risk when valuing all liabilities measured at fair value.

The methodology is consistent with that applied in developing

counterparty credit risk adjustments, but incorporates the

company’s own credit risk as observed in the credit default

swap market.

As an example, the fair value of derivatives is derived by a discounted

cash flow model using observable market inputs such as known

notional value amounts, yield curves, spot and forward exchange

rates as well as discount rates. These inputs relate to liquid, heavily

traded currencies with active markets which are available for the

full term of the derivative.

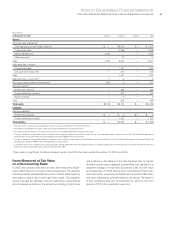

Certain financial assets are measured at fair value on a non-

recurring basis. These assets include equity method investments

that are recognized at fair value at the end of the period to the

extent that they are deemed to be other-than-temporarily impaired.

Certain assets that are measured at fair value on a recurring basis

can be subject to nonrecurring fair value measurements. These

assets include public cost method investments that are deemed

to be other-than-temporarily impaired. In the event of an other-

than-temporary impairment of a financial instrument, fair value is

measured using a model described above.

Accounting guidance permits the measurement of eligible

financial assets, financial liabilities and firm commitments at fair

value, on an instrument-by-instrument basis, that are otherwise not

permitted to be accounted for at fair value under other accounting

standards. This election is irrevocable. The company does not

apply the fair value option to any eligible assets or liabilities.

Cash Equivalents

All highly liquid investments with maturities of three months or less

at the date of purchase are considered to be cash equivalents.

Marketable Securities

Debt securities included in current assets represent securities that

are expected to be realized in cash within one year of the balance

sheet date. Long-term debt securities that are not expected to be

realized in cash within one year and alliance equity securities are

included in investments and sundry assets. Debt and marketable

equity securities are considered available for sale and are reported

at fair value with unrealized gains and losses, net of applicable

taxes, recorded in accumulated other comprehensive income/(loss),

a component of equity. The realized gains and losses for available-

for-sale securities are included in other (income) and expense in

the Consolidated Statement of Earnings. Realized gains and losses

are calculated based on the specific identification method.

In determining whether an other-than-temporary decline in

market value has occurred, the company considers the duration

that, and extent to which, the fair value of the investment is below

its cost, the financial condition and near-term prospects of the

issuer or underlying collateral of a security; and the company’s

intent and ability to retain the security in order to allow for an

anticipated recovery in fair value. Other-than-temporary declines

in fair value from amortized cost for available-for-sale equity and

debt securities that the company intends to sell or would more

likely than not be required to sell before the expected recovery of

the amortized cost basis are charged to other (income) and

expense in the period in which the loss occurs. For debt securities

that the company has no intent to sell and believes that it more

likely than not will not be required to sell prior to recovery, only the

credit loss component of the impairment is recognized in other

(income) and expense, while the remaining loss is recognized in

other comprehensive income/(loss). The credit loss component

recognized in other (income) and expense is identified as the

amount of the principal cash flows not expected to be received

over the remaining term of the debt security as projected using

the company’s cash flow projections.

Inventories

Raw materials, work in process and finished goods are stated at

the lower of average cost or market. Cash flows related to the sale

of inventories are reflected in net cash from operating activities in

the Consolidated Statement of Cash Flows.

Allowance for Credit Losses

Receivables are recorded concurrent with billing and shipment of

a product and/or delivery of a service to customers. A reasonable

estimate of probable net losses on the value of customer receivables

is recognized by establishing an allowance for credit losses.

Notes and Accounts Receivable—Trade

An allowance for uncollectible trade receivables is estimated based

on a combination of write-off history, aging analysis and any specific,

known troubled accounts.